Seaborne thermal coal prices jumped more than 25% in the first weeks after the Strait of Hormuz crisis, US coal consumption rose 10% in 2025, and prices are about 15% above pre-war levels.

The Iran shock has reopened export opportunities for coal miners, especially in the US, as global buyers scramble for fuel with the Strait of Hormuz still (as of April 22) closed.

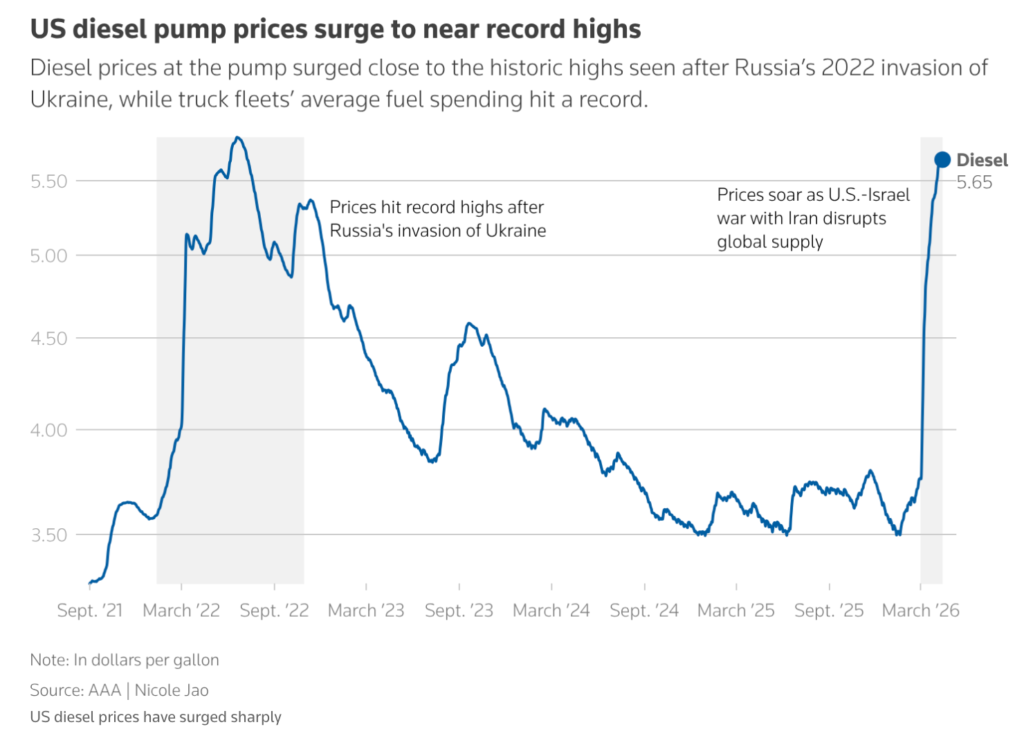

But, this is not a clean bull market. It is a geopolitical price spike running into a cost wall, as much of the upside is being taken up by higher mining, diesel and transport costs.

This distinction matters as price spike driven by war and fuel switching is not necessarily the same as a durable recovery in coal economics, unless of course, the closure of the Strait of Hormuz and recent destruction of fossil fuel energy infrastructure signals a long-term downgrade in energy exports from the Middle East.

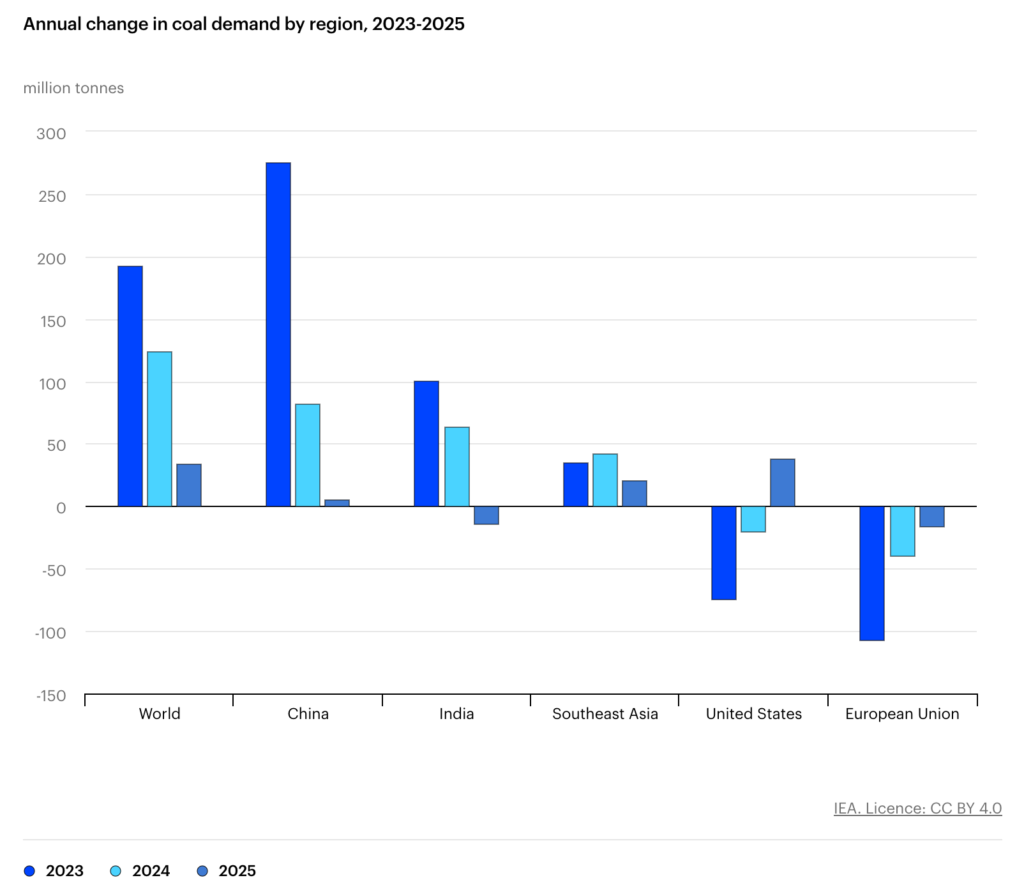

The IEA estimates global coal demand still edged higher in 2025, up 0.4%, even as growth slowed sharply from 2024. In the US, coal use in power was strong enough to support that 10% rise. Globally, however, the fuel is no longer in a real growth cycle. It is being propped up by disruptions, not by improving long-term fundamentals.

Logistics and production costs are eroding the miners profits, as the Iran conflict has pushed up fuel and transport costs across supply chains, while diesel prices have become a major burden in freight-heavy industries. In US trucking, diesel spending has already hit record highs. For coal, that matters twice: once at the mine and again on the way to port.

However, if diesel supply continues to tighten, then the price of coal will likely follow — as miners are simply unable to dig as much out of the ground.

The move comes after China’s coal-fired generation fell in 2025 for the first time since 2015, as renewables, hydro and nuclear absorbed more demand growth.

The question for the market now is whether this is only a trading rally, or a regime change in the face of a conflict in the Middle East.