Copper has hit prices $14,000 a tonne.

The metal rallied for an eighth straight session on Wednesday, touching $14,196.50/t on the London Metal Exchange, within sight of January’s all-time high of $14,527.50/t. It later traded around $14,099/t in Shanghai, according to Bloomberg.

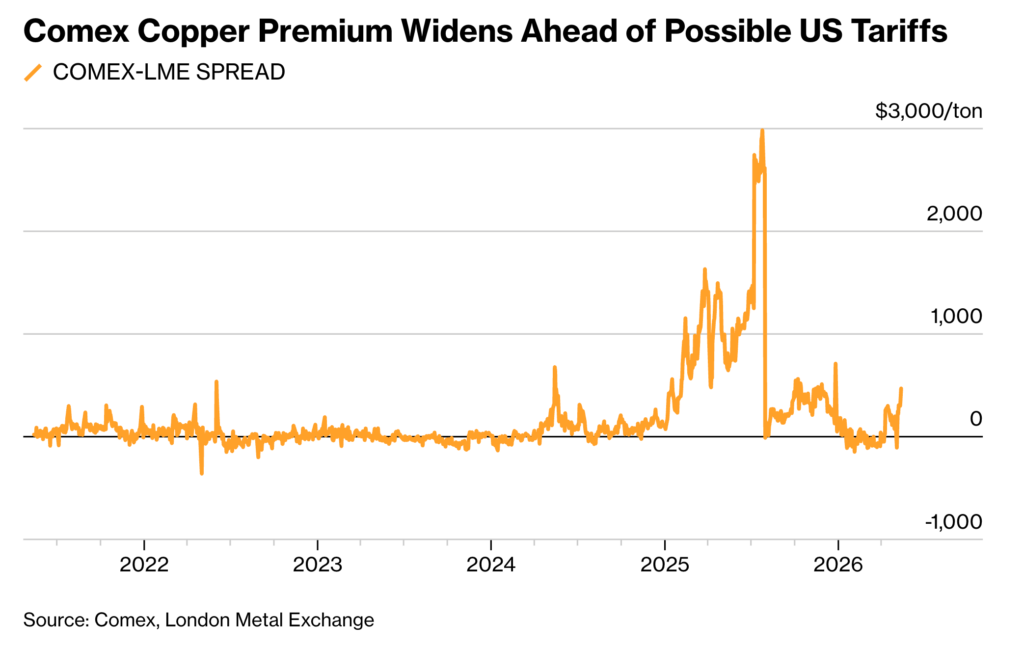

This is no longer just a “green transition” trade, but a supply stress trade.

In particular, sulphuric acid — a critical input for parts of the copper supply chain — has become a new chokepoint with the blockade of the Strait of Hormuz.

Goldman Sachs has warned that sulphuric acid shortages could threaten solvent extraction and electrowinning operations, which account for about 17% of global copper production. The bank has flagged particular risk in the Democratic Republic of Congo and Chile, two of the world’s most important copper jurisdictions.

Mine disruptions are also mounting, most recently the Grasberg mine disruption has added another layer of pressure with warnings any restart has been delayed until 2028. The Indonesian mine is one of the world’s largest copper operations, and delays to its recovery have tightened an already fragile market.

Here are the main copper mine disruptions from roughly 2023–2026, ranked by market relevance.

| Mine / region | Timing | Disruption | Why it matters |

|---|---|---|---|

| Cobre Panamá, Panama — First Quantum | Late 2023–present | Mine shut after protests and Panama Supreme Court ruling that the operating contract was unconstitutional. | One of the biggest shocks to copper supply. The mine accounted for about 1% of global copper output and remains closed, although Panama has allowed some stockpiled material to be processed/removed. |

| Grasberg, Indonesia — Freeport-McMoRan | Sept 2025–2026 | Deadly mudflow / wet muck incident halted operations and damaged underground infrastructure. | One of the world’s largest copper mines. Benchmark estimated 591,000 tonnes of lost copper output between Sept 2025 and end-2026; Goldman estimated 525,000 tonnes of mine-supply losses. Freeport now expects only 65% capacity in H2 2026, rising to near full output by end-2027. |

| Kamoa-Kakula, DRC — Ivanhoe/Zijin | May–June 2025 | Seismic activity and flooding forced partial suspension at Kakula. | Ivanhoe withdrew prior 2025 guidance of 520,000–580,000 tonnes and cut it to 370,000–420,000 tonnes. It also withdrew its 2026 target of about 600,000 tonnes. |

| Quebrada Blanca, Chile — Teck | 2024–2026 | Tailings disposal / embankment issues constrained ramp-up. | Teck cut 2025 QB copper guidance to 170,000–190,000 tonnes, down from 210,000–230,000 tonnes, and reduced 2026 guidance to 200,000–235,000 tonnes, down from 280,000–310,000 tonnes. |

| El Teniente, Chile — Codelco | July 2025 onward | Deadly collapse led to shutdowns and regulator conditions on restarts. | Codelco shut all sections after the accident, later reopening most areas, but some units remained closed. The company cut its copper production forecast because of the impact. |

| Las Bambas, Peru — MMG | Recurrent; latest major blockade Apr 2024 | Community protests blocked a key transport corridor. | Las Bambas normally supplies around 2% of global copper and has suffered more than 600 days of stoppages since starting operations in 2016. April 2024 blockades disrupted concentrate transport, though the mine used alternative routes. |

| Escondida, Chile — BHP | Aug 2024 | Strike at the world’s largest copper mine. | Short-lived, but market-moving. The main union suspended the strike after a revised wage offer; the strike had lifted copper prices on supply fears. |

| Chile national power outage — multiple mines | Feb 2025 | Major blackout knocked out power to mines in northern Chile. | Temporary rather than structural, but important because Chile is the world’s top copper producer. Reuters reported the outage hit major copper mines and moved global metals markets. |

| Codelco portfolio, Chile | 2023–2026 | Structural underperformance: grades, ageing assets, project delays and site-specific problems. | Codelco output hit a 25-year low in 2023 and remained under pressure in 2024; in 2025–26, increases at some mines offset declines from geological factors and El Teniente restrictions. |

| Altonorte smelter, Chile — Glencore | Mar 2025 | Force majeure on copper shipments after unexpected production suspension. | Not a mine, but a supply-chain disruption. Altonorte has capacity of about 350,000 tonnes of copper anodes a year, so the event mattered for refined supply. |

Market takeaway: copper’s problem is not one disruption. It is stacked disruption.

Panama removed around 1% of global supply. Grasberg added a half-million-tonne-plus supply hit. Kamoa-Kakula cut one of the key growth engines. Quebrada Blanca’s ramp-up disappointed. Codelco remains under structural strain. Peru keeps showing political risk.

That is why copper is trading like a supply-risk metal, not just a demand-growth metal.

Refined copper output in China fell to 1.05 million tonnes in April, down 3% from March, with production potentially falling further in May because of smelter maintenance.

The copper bull case has become simple: demand keeps broadening, while supply keeps failing to respond fast enough. Power grids, electric vehicles, data centres, AI infrastructure, defence electrification and industrial reshoring are all pulling on the same metal at the same time.

The market needs ore, concentrate, smelting capacity, acid, power, transport and permits to work together. Instead, bottlenecks are appearing across the chain.

That is the market’s new vulnerability. Copper supply is no longer just about digging more rock. It is about whether the industrial inputs needed to turn that rock into metal are available, affordable and secure.

And, the demand side is not waiting.

UBS projects global copper demand to grow 2.8% in both 2025 and 2026, supported by EVs, renewable energy, power grids and data centres. But it also cut refined copper production growth estimates, citing grade declines and operational challenges.

That is the core imbalance: Demand growth is becoming more diversified as supply growth is becoming more conditional.