📌 Key Takeaways

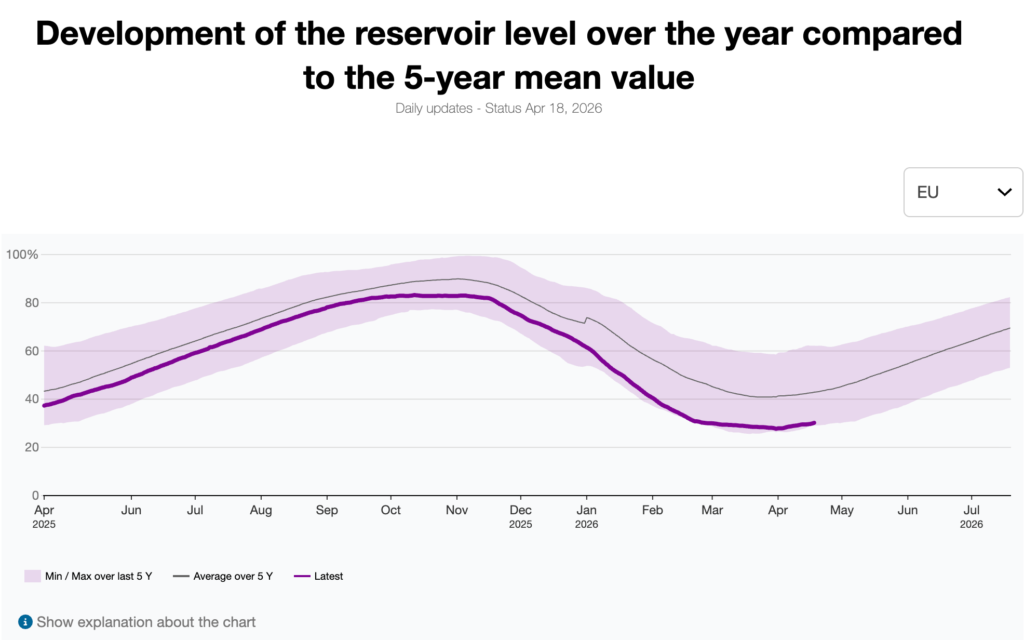

- EU gas storage was 28.9% full on April 10, the lowest level for that date since 2021.

- Europe may need to inject more than 60 bcm this summer to meet the EU’s winter storage rule.

- European gas prices increased more than 70% between February and March, while Qatari LNG remains badly disrupted.

- The issue is not just Europe’s direct exposure to Qatar. It is that Europe now has to refill storage in a tighter global LNG market.

EU gas storage is back in the danger zone. Underground inventories across the bloc were 28.9% full on April 10, according to AGSI data, the lowest level for that point in the calendar in five years, as European storage drops below 30% — all just as Europe’s refill season starts.

The problem is not just the closure of the Strait of Hormuz, trapping both LNG exports and LNG tankers, but the damage done to Middle East natural gas facilities, including Iranian attacks knocking out 17% of Qatar’s liquefied natural gas (LNG) export capacity, causing an estimated $20 billion in lost annual revenue and threatening supplies to Europe and Asia.

That matters because Europe is not trying to refill from a position of comfort. Under the EU’s extended gas storage regime, member states are still expected to reach 90% filling sometime between October 1 and December 1, even though Brussels has added more flexibility around the target. Eurogas said in March that, to meet that rule, market participants may need to inject more than 60 bcm this summer. That is a very large refill job in any year. In a year when LNG supply is disrupted and prices are already elevated, it becomes a market stress test.

The conflict in the Middle East does not mean Europe loses all of its gas overnight. Europe secured only 7% of its LNG supplies from Qatar in 2025, with Qatar accounting for 3.5% of total EU gas supply in 2025. The deeper problem is that Qatari LNG is a core balancing molecule for the global system. When that supply is impaired, Europe has to compete harder for every spare cargo.

Where can Europe get the gas instead?

That is the central question, and there is no clean answer.

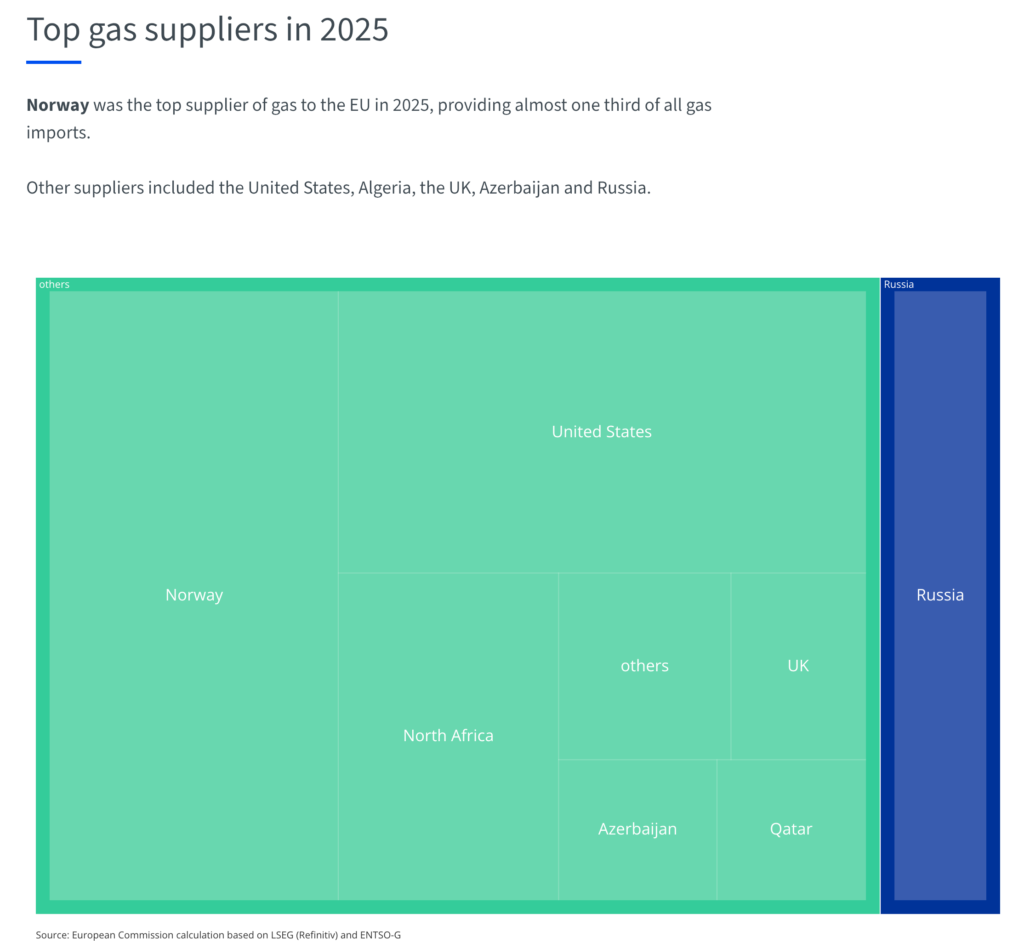

Norway remains Europe’s largest gas supplier, accounting for more than one-third of supply, but it cannot simply ramp output at will. The United States became the EU’s top LNG source in 2025, supplying 25% of EU LNG imports, and IEA expects Europe’s LNG imports to rise again in 2026 to a record more than 185 bcm. But, as we’ve reported, even that comes with limits: U.S. facilities were already running hard, while the IEA said Europe’s higher storage injection needs were a major reason LNG demand would keep climbing this year.

Instead, Europe has increase imports from Russia, with the EU taking 97% of the cargoes from the vast Yamal LNG project in Siberia in the first three months of year. eg Spain imported a record 9,807 GWh of Russian liquefied natural gas in March.

Italy’s Edison has already moved to replace canceled Qatari volumes with seven U.S. cargoes, after QatarEnergy canceled 10 shipments totaling 1.4 bcm under force majeure. That is a live example of where Europe will look next: more U.S. LNG, more spot competition, and more price sensitivity.

The problem is that extra supply for Europe is not the same as cheap supply for Europe. Every replacement cargo has to be bid away from someone else.

Does this mean another 2022-style gas crisis?

Not yet. But it does mean Europe is more exposed than markets were assuming.

Reuters reported in March that Dutch benchmark gas had reached €74/MWh, roughly double where it stood before the conflict, though still far below the peaks above €300/MWh seen in 2022. In other words, this is not yet a full repeat of the old crisis. But the refill season has started from a weaker base, with tighter supply, and with less room for complacency.

The European Commission’s own message has shifted in that direction. It has urged countries to begin filling early, while also building more flexibility into the storage framework so governments are not forced to buy at the worst possible moment. That tells you Brussels sees a real tension between security of supply and price discipline.

What does EU gas storage mean now?

It means Europe has lost its margin of safety.

Storage near 30% in April is not a crisis by itself. The crisis is what it forces Europe to do next. The bloc now has to buy tens of billions of cubic meters of gas into storage while Hormuz remains unstable, Qatari LNG is constrained, and alternative supply is finite. That is why gas storage is no longer just a winter insurance story. It is the mechanism through which a Middle East shock gets priced into European industry, power markets, inflation, and policy.

For investors, the message is simple. Europe does not need to run out of gas for this to matter. It only needs to keep refilling from a position of weakness. In that setup, every cargo matters, every outage matters, and every geopolitical headline gets amplified through the storage curve.