📌 Key Takeaways

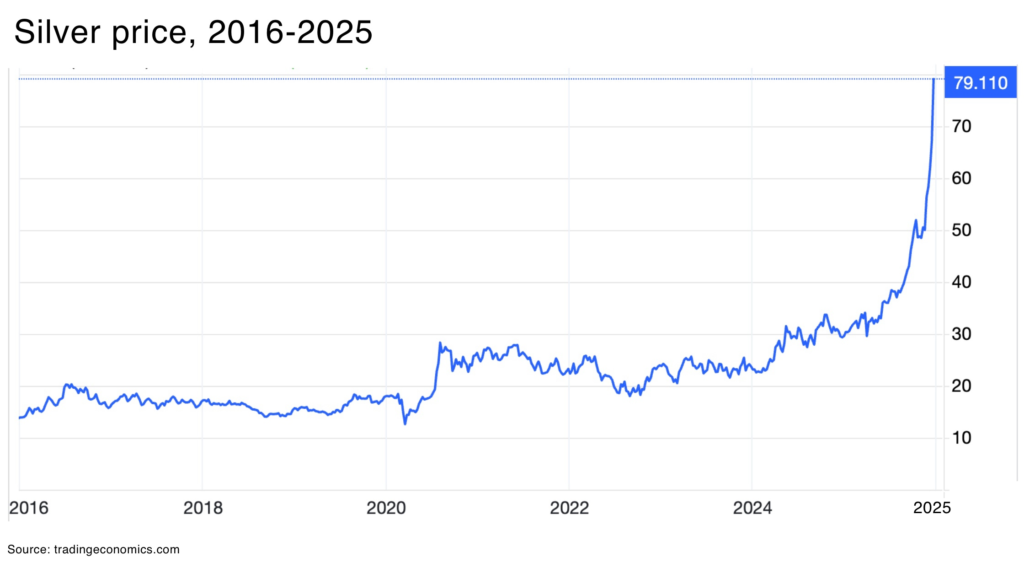

- Surging Prices: The silver price ended 2025 above $65/oz (a 120% year-to-date gain), far outpacing gold’s 64% rise.

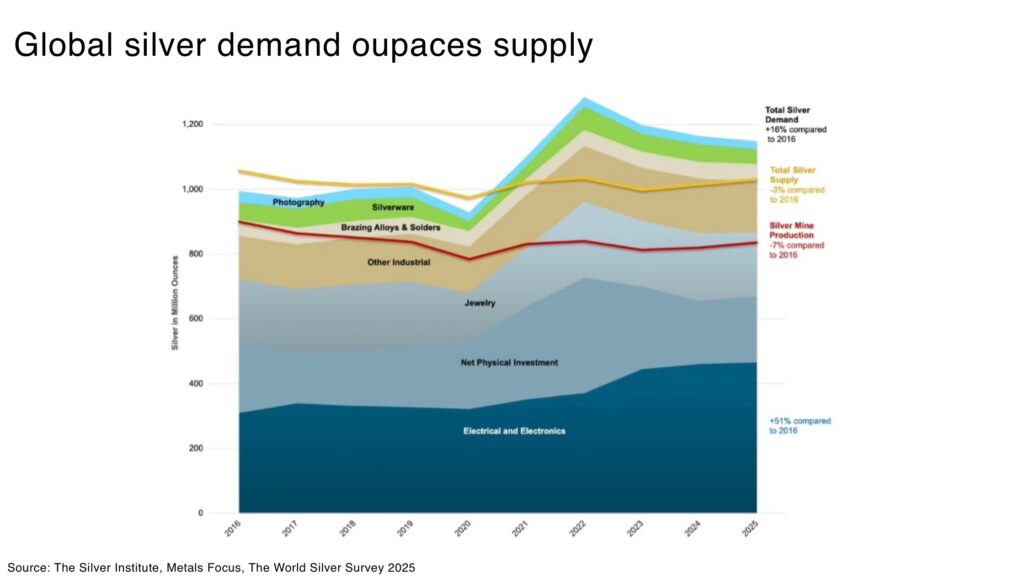

- Structural Supply Deficit: 2025 will mark five consecutive years of silver supply deficits.

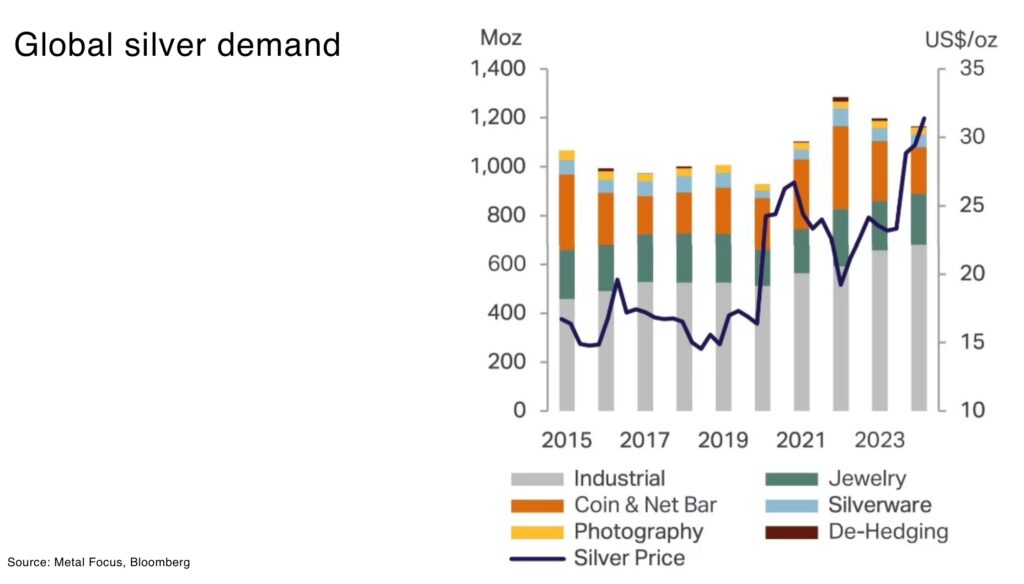

- Demand Boom from Industry: Industrial use hit a record 680.5 Moz in 2024, driven by solar panels, electric vehicles (EVs), and electronics.

- Investor Rush & Tight Supply: Silver-backed ETF holdings surged approx 40% in 2025, and global mints struggled to meet coin demand amid a physical squeeze. Exchange inventories slid to multi-year lows as metal flowed to Asia, pushing silver lease rates above 5% (vs 0% typical).

Silver’s 2025 rally has been historic. By December, prices vaulted above $65 per ounce, more than doubling from January. This meteoric rise reflects a perfect storm of forces: structural supply deficits, surging industrial demand, and safe-haven investment flows.

The current parabolic move shows signs of mania versus fundamentals, but those market fundamentals are still bullish.

Silver now straddles two worlds – both an industrial metal and a monetary metal – giving it a unique role among critical minerals. And, in 2025, the U.S. added silver to its official Critical Minerals list.

So, the question on every silver investor’s mind: how high can silver go?

Let’s look at some of the fundamentals, and then into some of the events that means the price is spiking — and where the price goes from here.

How is Industry driving Silver Demand?

Industrial demand for silver is hitting all-time highs, thanks to relentless growth in high-tech and energy transition applications. In 2024, global industrial silver consumption reached ~680.5 million ounces – a new record – even amid broader economic headwinds.

This means more than half of total silver demand now comes from industry, with three main drivers leading the charge:

- Solar Photovoltaics (PV): Silver’s superior electrical conductivity makes it essential in solar panels. As solar deployment has exploded (installed PV capacity is over 10× higher than in 2013 ), silver demand for solar cells has nearly quadrupled in that time. In 2024, roughly 25% of global silver consumption came from the solar sector.

And, looking ahead, solar’s appetite for silver is set to grow further, with projections estimating PV-sector silver demand could rise by as much as 170% by 2030. The International Energy Agency forecasts global solar capacity to expand by more than 3,600 GW by 2030. - Electric Vehicles (EVs) and Electrification: Modern vehicles are effectively “computers on wheels,” heavily reliant on electronics – and thereby on silver. Battery EVs use on average 70% more silver per car than internal combustion vehicles, due to silver’s use in battery management systems, inverters, charging ports, and numerous sensors.

The Silver Institute forecasts automotive silver demand to grow ~3.4% annually from 2025–2031, with EVs overtaking traditional cars as the dominant source of auto-sector silver demand by 2027. By 2031, EVs and their charging infrastructure are expected to account for ~59% of automotive silver usage.

And the horizon extends well beyond 2030 – by 2040, EVs alone could require nearly half of the world’s silver output if current trends continue. - Semiconductors, Data Centers & 5G/AI Infrastructure: Silver’s role as the most conductive metal also makes it critical in advanced electronics and communications. Data centers and cloud computing hardware rely on silver in numerous components, from multi-layer ceramic capacitors to circuit board coatings. The rise of artificial intelligence (AI) and big data is turbocharging the construction of server farms and network infrastructure. Total global IT/data center power capacity has increased 53-fold since 2000 a proxy for how much more hardware (and thus silver-bearing electronics) the digital economy now requires.

Similarly, 5G networks and next-gen telecom equipment use silver in connectors and solder. As these trends accelerate, silver is solidifying its status as a “technology metal.” Over the coming decade, the continued digitization and electrification of everything from smart grids to cloud computing should keep industrial silver demand on a steady upward climb.

The range of sectors that need silver means that, even in years of slow growth in one industry, the demand portfolio is diversifed enough to keep the silver price resilient.

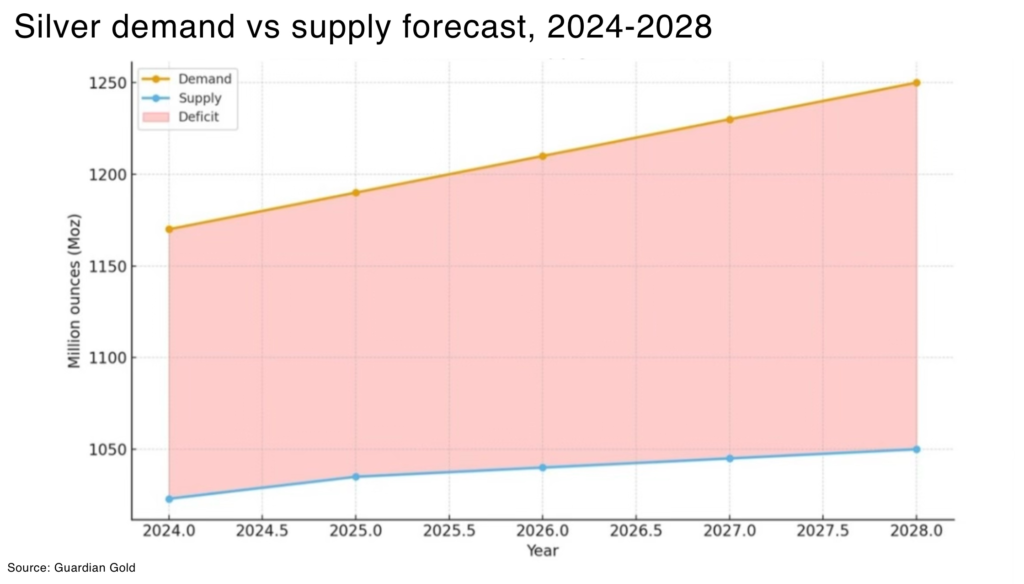

This structural demand growth is fundamentally reshaping the silver outlook. The Silver Institute projects global silver demand will stay above 1.1 billion ounces in 2025 – an unusually high plateau historically – driven largely by these technology sectors (alongside steady jewelry and silverware use). Industrial demand alone is expected to climb from 680 Moz in 2024 to over 750 Moz by 2028.

In other words, industrial trends (solar adoption, EVs, automation) are effectively raising the floor for silver consumption — and the fundamental moving the price is that supply is not keeping up.

Why Is the Silver Market in a Deficit?

The silver market has been in a structural supply deficit for the past seven years, as mine production struggles to keep pace with surging demand. Starting in 2021, total silver demand began exceeding annual supply, and the gap has widened into a multi-year squeeze. The major causes of the supply crunch include:

- Falling Mine Output: Global silver mine production peaked in 2016 at around 900 Moz, and it has drifted lower since. In 2024, mine output was just 820–840 Moz, and 2025 is estimated at 835 Moz, still well below the last decade’s highs. But, despite elevated prices, miners have not been able to significantly boost output.

In part this is because most silver (approx 70%) is produced as a byproduct of mining other metals (e.g. lead, zinc, copper, gold). Higher silver prices don’t easily translate into more supply when silver is a secondary product. A zinc mine, for example, won’t double output just because silver prices rise. Roughly 28% of silver comes from primary silver mines, and many of those face rising costs and grade declines.

Moreover, after years of under-investment, there’s a dearth of new projects in the pipeline – developing a new large mine can take 10–18 years from discovery to production. The result is a relatively inelastic supply profile: even as demand surges, mine supply is inching up only modestly. Mineral ore reserves at primary silver mines grew 2.4% y/y or 83.3Moz (2,591t) in 2024. - Structural Deficits: The persistence of shortage conditions is striking. Total silver supply (mine + recycling) has been below total demand each year since 2021. In 2022 the shortfall blew out to ~253 Moz – the largest deficit on record – amid a post-pandemic surge in consumption. The cumulative silver deficit from 2021–2025 reached 678 Moz, roughly equivalent to 10 months of mine production — not including the expected deficit for 2025 and 2026.

This means a significant amount of silver above-ground stocks have been drawn down to satisfy consumption in recent years. These sustained shortfalls are unprecedented in modern times for silver. They underscore that this is not a one-off imbalance but a structural issue where demand growth has outstripped what supply can deliver.

- Limited Near-Term Relief: Looking forward, silver supply growth is expected to remain limited. A few new mines or expansions (in places like Mexico and Australia) are adding ounces, but they barely offset declines elsewhere. Recycling provides 15–20% of total supply (194 Moz in 2024), and while high prices have encouraged slightly more scrap recovery, it’s not a game-changer.

The upshot: even under conservative demand forecasts, some estimates suggest annual deficits on the order of 100 Moz or more could persist well into the late 2020s.

Supply Squeeze by the Numbers:

- 5 – Consecutive years of global silver supply deficits (2021–2025) , an unprecedented streak in modern times.

- ~820 Moz vs 1,170 Moz – 2024 mine production (~820 million oz) vs total demand (~1,170 Moz), yielding a ~150 Moz market deficit.

- 678 Moz – Cumulative deficit from 2021–2024, equal to ~10 months of mine output. By 2025 the five-year total shortfall nears 820 Moz.

- 18 years – Typical timeline to discover, permit, finance, and commission a new major silver mine. Supply response is anything but quick, even at higher prices.

Why is Finance Flocking to Silver?

Beyond strong industrial usage, investment demand has been a major accelerant in silver’s 2025 rally. In an environment of rising economic uncertainty, silver benefits from its dual status as a precious metal safe-haven:

- Monetary Policy and the “Debasement Trade”: In 2025, the U.S. Federal Reserve shifted from aggressive tightening to rate cuts as inflation persisted and growth cooled. Real interest rates fell and the dollar weakened, reviving the classic “currency debasement” trade (across both the dollar and yuan) – fleeing paper money for hard assets. Investors fearful of eroding purchasing power poured into precious metals. This is particularly the case as crypto and bitcoin see big reversals. Gold’s headline-grabbing rise above $4,300/oz in 2025 (an all-time high) led these concerns – but silver has since outpaced gold. Once momentum took hold, silver’s smaller market size meant inflows had an outsized impact on price.

In short, the global backdrop of high inflation, rising debts, and geopolitical strife created a perfect recipe for safe-haven demand, and silver drew a lot of that interest. - Geopolitical Risk and Safe Havens: Turbulent geopolitics amplify the flight to safety. Investors typically seek shelter in precious metals during times of crisis. For markets, 2025’s flashpoints mattered less for headlines than for flow disruption: prolonged war in Eastern Europe, expanding U.S.–China export controls, repeated threats to global shipping lanes, and rising political risk in major mining jurisdictions.

- Investor Flows – ETFs and Coins: The data bear out this surge in investment demand. Global holdings of silver in exchange-traded funds (ETFs) jumped sharply in 2025. The World Gold Council and Metals Focus report that silver now comprises 7% of all precious metals ETF holdings globally, up from 4% in 2020. The value of these holdings also hit an all-time high above $40 billion as prices rallied.

Global Silver Stash: Who’s Buying? (Retail investment in silver has boomed across key markets)

- United States: The largest retail silver market. U.S. investors bought a combined 1.5 billion ounces of silver from 2010–2024 (about 46,600 tonnes), and most of that is still held in private hands. 2025 continued to see strong U.S. coin demand, though some Americans sold into price strength (taking profits).

- India: A traditional stronghold of silver ownership. Indian citizens purchased 840 Moz of silver in bar and coin form between 2010 and 2024. Even at record rupee prices in 2023–25, selling-back remained modest – Indians prefer to buy and hold silver as long-term wealth.

- Germany: Europe’s top silver stackers. German retail investment averaged an “eye-watering” 48.5 Moz per year in 2020–2022, as zero/negative interest rates and inflation fears drove savers into bullion. A tax change slowed demand in 2023, but 2024 saw a partial rebound with ~25% growth amid economic uncertainties.

- Australia: A rapidly growing market. Annual Aussie silver coin/bar demand leapt from 3 Moz in 2019 to a record 20.7 Moz in 2022. Contributing factors include rising interest in precious metals for retirement accounts and a favorable tax treatment. 2025 has remained strong as inflation moderates and investors hold tight to their silver.

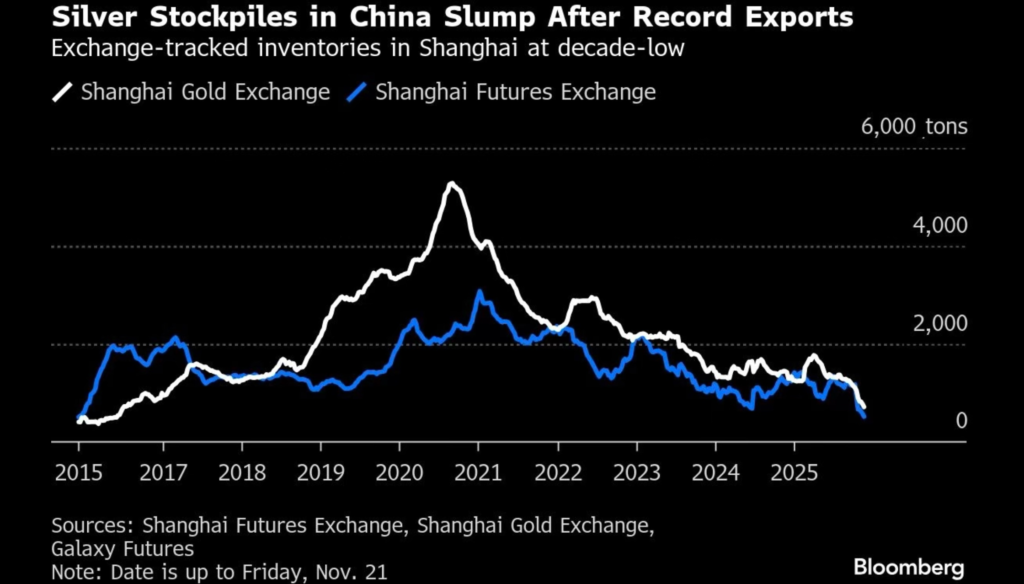

- Tight Physical Markets (Inventory Strain): One clear signal of the physical tightness caused by these trends has been the drawdown in silver inventories. Major trading hubs have seen stockpiles tumble. By late 2025, registered silver stocks in Shanghai fell to their lowest levels since 2015, and London vault holdings (a key storage center for ETFs and industry) also saw significant declines.

Sponsored Case Study: Why Apollo Silver Is Leveraged to a Structural Silver Bull Market

For investors looking to translate a structurally bullish silver setup into equity exposure, Apollo Silver Corp (TSX.V:APGO / OTCQB:APGOF) offers a high-beta option tied directly to primary silver supply rather than by-product production.

Apollo controls two advanced silver assets in tier-one jurisdictions, with its flagship Calico project located in the USA and Cinco de Mayo project in Mexico -regions with long mining histories, established infrastructure, and clear permitting frameworks. That jurisdictional profile matters in a market where new silver supply is scarce and geopolitical risk is increasingly priced into metals markets.

In 2025 Apollo, reported an updated Mineral Resource Estimate for Calico that reflected a 61% increase in tonnage and a 14% increase in contained silver ounces compared with the Company’s prior estimate. An updated NI 43-101 technical report (effective June 30, 2025) shows the Waterloo deposit, using a 47 g/t silver equivalent cut-off grade, includes 125 M oz of silver in in 55Mt at an average grade of 71 g/t silver in the Measured and Indicated categories, and 0.51 Moz silver in 0.6 Mt at an average of 26 g/t silver in the Inferred category. The Langtry Deposit now contains 57 Moz silver in 24 Mt at an average grade of 73 g/t in the Inferred category, using a 43 g/t silver cut-off grade.

Apollo’s focus is on primary silver systems. That distinction is critical. In a sustained silver bull market, primary producers and near-term developers tend to exhibit greater operational and valuation leverage to rising prices, as higher silver prices directly improve project economics rather than being incidental to another metal cycle.

In late 2025 the company announced a $25 million strategic private placement with cornerstone participation from Eric Sprott and Jupiter Asset Management, reinforcing shareholder alignment and providing capital for Calico drilling and development programs through 2026. And, on December 29 2025, company announced a $2.5 million upsizing to the financing to allow for insider participation.

Apollo’s projects sit within historic silver belts and brownfield districts, offering scale, geological continuity, and optionality. From a macro perspective, Apollo is exposed to several of the same forces driving the silver price higher:

- Structural supply deficits that limit new mine development.

- Rising strategic importance of silver as both an industrial and monetary metal.

- Capital scarcity for junior miners following years of underinvestment, which amplifies the value of advanced-stage projects as prices rise.

What Would It Take for Silver to Hit $100?

With silver now in uncharted price territory after 2025’s explosive run, a natural question arises: how much higher can it go?

On January 1st 2026, China will be imposing export restrictions on silver. Companies seeking export licenses must meet strict requirements including annual production of at least 80 tonnes.

This is a problem when China controls 70-80% of global silver supply.

This has led speculation by bulls that the price could reach the elusive $100/oz milestone – a level that not long ago seemed far-fetched.

Barring some massive economic downturn, industrial demand has raised the silver price floor, but reaching triple-digit silver may require a confluence of factors.

Baseline Outlook: Most mainstream analysts remain optimistic but not yet ready to predict $100 silver in the near term. For 2026, many forecasts cluster in the $60–$80 range.

Bull Case: The bulls argue that the ingredients for a melt-up are in place, and only need to intensify. They point out that in past precious metal bull markets, silver has demonstrated a tendency to overshoot (during 2008–2011, for example, the silver price rocketed by 431%). So, for example, a major supply shock in Mexico (approx 25% of global supply) or Peru would likely panic the market over supply; or if a key byproduct metal (like zinc or lead) saw production cuts for unrelated reasons, silver supply would inadvertently tighten; or, a severe currency crisis, inflation, or loss of confidence in central banks could ignite another wave of safe-haven buying.

What Could Hold Silver Back: The very factors that drive silver up can reverse quickly. For example, any sign of cooling inflation or a more hawkish policy by Central Banks turn could strengthen currencies and raise real interest rates, diminishing the appeal of precious metals; or further setbacks for renewable energy that impacts solar demand.

In particular, caution is always needed in sharp spikes, especially as this historically volatile metal remains vulnerable to steep corrections. China, as a net importer of silver, has little reason to want to see prices spike so quickly.

Conclusion – The Long-Term Context:

For investors and policymakers, the key takeaway is that the structural forces underpinning silver’s value are real and persistent. A sustained supply/demand imbalance appears likely to carry into the late 2020s and even 2030s, barring a major disruption in either supply or demand.