📌 Key Takeaways

- Over 60% of global critical mineral demand is met through international trade, creating structural interdependence between producers and consumers

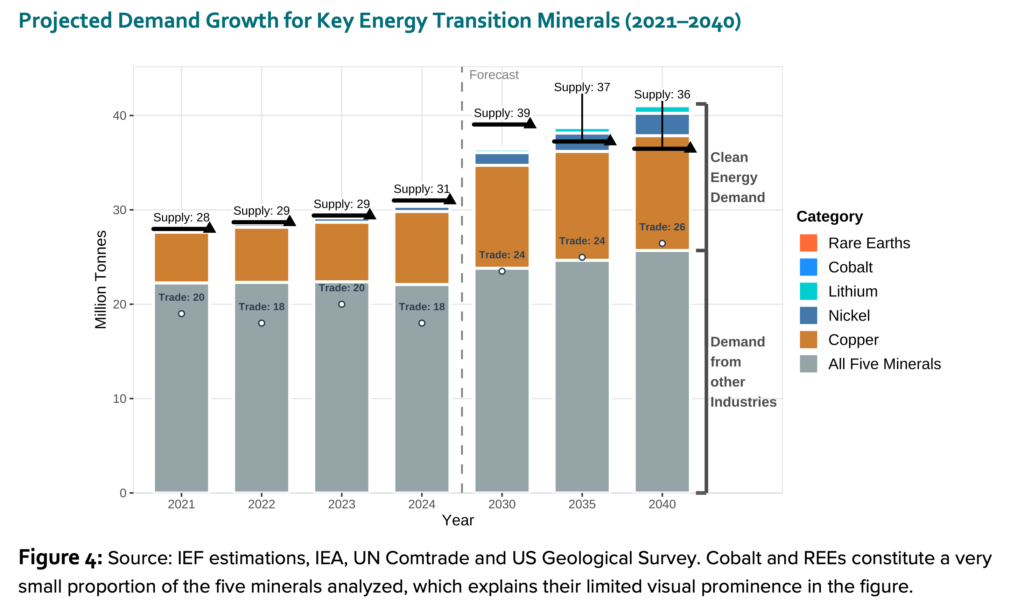

- Clean energy demand pushes total mineral demand from ~28 Mt (2021) to ~41 Mt by 2040, tightening supply chains

- Trade concentration is highest in lithium, cobalt, nickel and rare earths, amplifying geopolitical and policy risk

- Policy intervention since 2020 has nearly doubled versus the prior two decades, reshaping investment risk and opportunity

More than 60% of global critical mineral demand is met through international trade, underscoring how dependent the energy transition has become on cross-border — and potentially — fragile supply chains.

The dependence is not abstract. It is structural. As electric vehicles, grids, batteries and data centres scale, the materials that underpin them increasingly cross borders multiple times before reaching end users. The IEF estimates demand for key energy-transition minerals rises from ~28 million tonnes in 2021 to nearly 41 million tonnes by 2040, tightening supply chains already exposed to policy shocks and logistics bottlenecks.

For example, more than 900 copper mines, smelters and refineries are currently in operation worldwide, spanning a wide range of production confidence levels, from low associated with early stage, informal or poorly documented operations to high reflecting long established and fully operational facilities. Approximately one third of these mines are in the Americas.

The interdependency comes as demand for these critical minerals continues to rise, driven by the material requirements of global energy system transformations. Total global demand increases from roughly 28 mega tonnes (Mt) in 2021 to nearly 41 Mt by 2040, highlighting the growing dependence of clean energy technologies on mineral-intensive supply chains:

- copper remains the dominant component, more than doubling to exceed 12 Mt

- lithium and nickel record the fastest growth, expanding more than tenfold as their roles in electric vehicle batteries and energy storage systems deepen

- iREEs and cobalt show steady but moderate increases, reflecting their indispensable use in high-efficiency motors, electronics, and advanced manufacturing

Clean energy amplifies the risk. Electric vehicles use roughly four times more copper than internal-combustion cars. Battery demand drives lithium and nickel consumption up more than tenfold by 2040. Offshore wind alone requires tens of thousands of tonnes of critical minerals per gigawatt. Yet new mines typically take 13–23 years to reach production, leaving trade as the system’s pressure valve — and its point of failure.

“Critical minerals are no longer a niche issue at the margins of the energy transition, they are now central to energy security, economic competitiveness, and the credibility of national climate strategies. Without secure, transparent, and resilient mineral supply chains, the energy transition itself is at risk” —Jassim Alshirawi, Secretary General, IEF

Governments are responding. The IEF tracks more than 600 critical-minerals policies globally, with activity since 2020 nearly double that of the previous two decades. Strategic planning still dominates, but trade controls and export restrictions are rising faster than environmental policy, reshaping investment risk and returns .

The IEF argues that producer–consumer dialogue can temper volatility, pointing to decades of oil-market coordination that improved transparency and crisis response. Applied to critical minerals, sustained dialogue anchored in data could align expectations on supply, refining capacity and investment timing. Without it, fragmentation increases — and so does the cost of capital.

The takeaway for markets is blunt. The energy transition is not demand-constrained. It is trade-constrained. With more than 60% of critical minerals flowing across borders, resilience now hinges on diversified supply, predictable trade rules and investable jurisdictions that reduce concentration risk.