- ⛏️ Silver is now a precious, industrial — and critical metal.

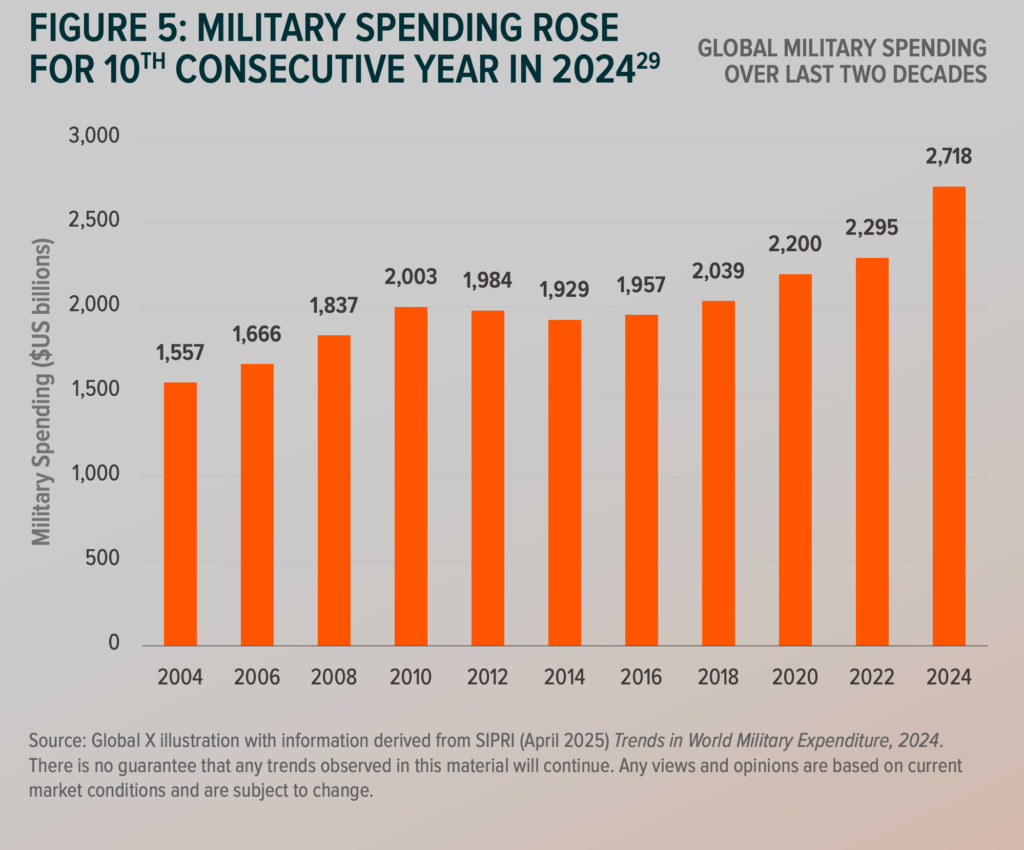

Global military expenditure reached $2.718 trillion in 2024, an increase of 9.4% from 2023, the steepest one-year surge since the Cold War.

From precision-guided munitions to stealth aircraft and advanced radar, all are dependent on the unique physpcial properties of silver — the highest electrical and thermal conductivity of all elements — make it foundational to the new arms race.

Silver has transitioned from, not just a precious metal to industrial metal, but now a critical mineral. With the market facing its fifth consecutive year of structural deficit, military demand is no longer just a “side story”, it is the catalyst for a potential supply crisis.

🚨 The “Sticky” Demand of Modern Warfare

Unlike the cyclical nature of consumer electronics or jewelry, military procurement operates on long-term, multi-decade budgets. This creates sticky demand that is largely insulated from economic downturns. A manufacturer will not design silver out of a multimillion-dollar weapon system even if the metal’s price doubles, as the reliability of a $2 million missile cannot be compromised.

Military needs for silver include electricity conductivity, corrosion resistance, reflectivity and heat conducivity.

The amount of silver used in military equipment is highly classified, so exact estimates are unknown, but to provide an idea of the scale silver is essential across munitions and high-tech infrastructure:

- Tomahawk Missiles: A single Tomahawk cruise missile requires an estimated 15 ounces (some estimates suggest as high as 500 ounces) of silver for its guidance system circuitry and high-reliability silver-zinc batteries. The U.S. currently maintains thousands of Tomahawks in its stockpile. This program alone, estimates the CPM Group, has consumed roughly 32,000 ounces of silver over the last 40 years, with another 120,000 ounces currently locked in inventory and unavailable to the market.

- At today’s production rates, that is only around 0.02% of annual global mine supply, which is expected to be in the 800–900 million ounce range, but the point is not the percentage in isolation: this is a single program, for a single class of missile, in a single country. In a world where global mine output is stagnating and multiple nations are simultaneously rearming across missiles, drones, radar and electronic warfare systems, the cumulative impact of dozens of such programs becomes material to a market already running persistent structural deficits

- Radar and Surveillance: Aegis-class naval radar systems incorporate large volumes of silver-plated contacts, cabling and RF components, tying up significant quantities of silver over multi-decade service lives.

- Aviation: The F-35 stealth fighter utilizes silver in its radar-absorbent wiring and advanced sensor suites.

- Drones: High-reliability MIL-spec connectors and camera systems rely on silver-plated components and silvered mirrors to ensure low contact resistance and maximum reflectivity for night-vision targeting.

- Other Applications: include satellites, tanks, night-vision goggles, communication devices, and space technology

A critical supply–demand factor for silver used in munitions is that, once the weapons are deployed, the metal is permanently removed from the market, as it is no longer retrievable at scale. Unlike a silver ring or an industrial contact that can be recycled, silver in a missile is shattered or lost on the battlefield. This is a “one-way street” for supply.

📈 The Structural Squeeze

The defense sector’s growing appetite for silver is hitting a market that is already historically structurally tight. Entering 2026, the silver market is grappling with a 5 year structural deficit that is being exacerbated by three primary industrial drivers:

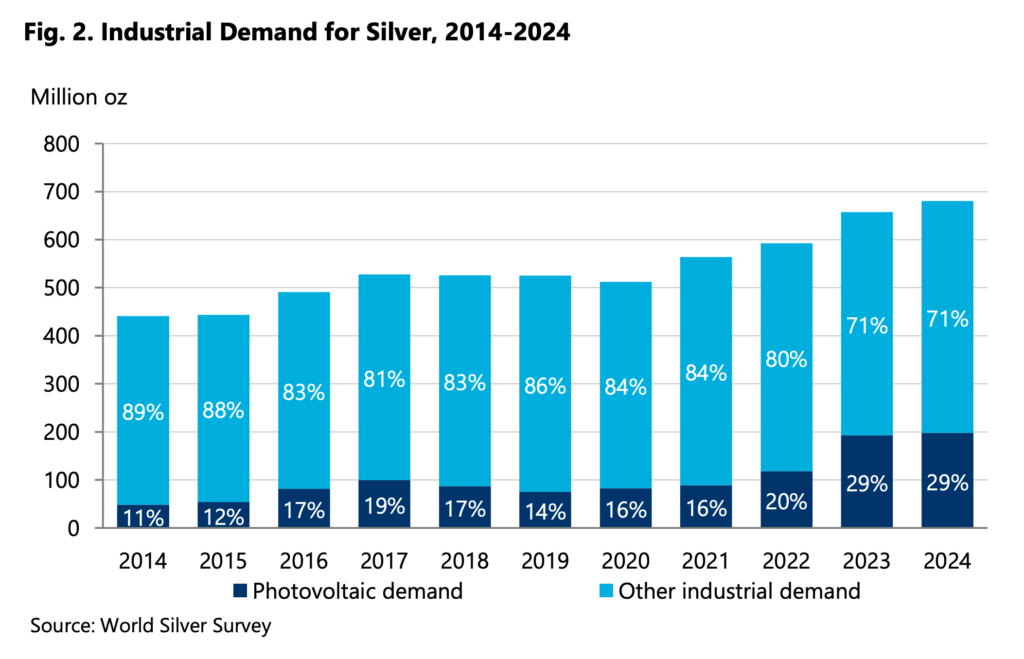

- Solar Photovoltaics: in 2014, only 11% of silver industrial demand was consumed in this sector, compared to 29% in 2024, reaching 232 million ounces. Next-generation TOPCon solar technology, which is rapidly becoming the industry standard, requires up to 50% more silver per panel than traditional cells.

- Electric Vehicles (EVs): Modern EVs utilize up to 79% more silver than internal combustion engine vehicles for battery management, power electronics, and sensors. Automotive silver demand is projected to reach approximately 94 million ounces annually by 2031, with EVs overtaking ICEs as the primary source by 2027.

- AI and Data Centers: The expansion of global IT power capacity, up 53x since 2000, has created a new, massive demand for silver-intensive switches, servers, and cooling systems essential for AI hardware.

“Global silver industrial demand is poised to grow further as demand from vital technology sectors accelerates over the next five years. Sectors such as solar energy (PV), automotive electric vehicles (EVs) and their infrastructure, and data centers and artificial intelligence (AI) will drive industrial demand higher through 2030” — The Silver Institute, Silver Demand Forecast, Dec 9 2025

🪙 The Silver Inventory Wall

The cumulative effect of these drivers is staggering on the silver market. Since 2021, the world has consumed nearly 820 million ounces of silver more than it has produced.

- Inventory Erosion: Above-ground stocks in London, New York and Shanghai are being drained to fill the gap, threatening to leave the market with no “lender of last resort”.

- Supply Inelasticity: 70% of silver is mined as a byproduct of other metals like copper, lead, and zinc. This means silver production cannot easily ramp up to meet price signals, as it depends on the economics of larger mining operations.

Strategic Vulnerability

Highlighting this urgency, the US Geological Survey recently added silver to its critical minerals list, acknowledging its role as a strategic resource. This priorities security of supply over certain free market principles.

And US policy is responding with President Trump’s administration shifting decisively toward securing critical mineral supply chains, including:

- $2 billion for National Defense Stockpile purchases

- $5 billion for the Industrial Base Fund

- $500 million for defense credit program

- and direct investment into mining companies, from MP Materials to Korea Zinc, Lithium Americas to Trilogy Metals

National security demands are creating a more favourable backdrop for advancing projects that can contribute to domestic supply resilience at a time when silver is being reclassified from a mere precious/industrial metal toward a strategic input for energy, technology and national defense.

🔫 Structural Shift: Defense Demand That’s Here to Stay

For decades, silver demand rose and fell with the business cycle, driven by swings in electronics, solar, installation booms, or jewelry buying sprees. Defense was a small player, often overlooked, but geopolitical realities have forced a step-change in how countries spend on defense, and by extension how they consume critical materials.

Military demand for silver is increasingly structural demand driver — that is also largely recession proof once the defence contract for new fighters or missile defence systems are locked in.

The scale of silver in defense is still likely very modest relative to total demand from other drivers, however its inelastic nature in a market already so tight will mean it carries outsized influence.

Also, the hidden nature of the demand increases volatility as any significant increase in demand cannot be anticipated.

The U.S. Defense Department stopped disclosing silver usage in the 1990s. That opacity means potential sudden impacts: a major conflict or new weapons program (or, conversely, a diplomatic breakthrough) could materially tighten the silver market without much warning.

For example, it’s possible to see very large, unexpected demands: to construct the first atomic bomb, the U.S. Treasury loaned the Manhatten Project 14,700 tons of the precious metal from the reserve, which was then shaped into suitable parts. (After the war all the silver was melted down and returned, with less than 1% lost)

—

Sponsored Case Study: Why Apollo Silver Is Strategically Positioned

Apollo Silver TSX.V:APGO / OTCQB:APGOF offers direct exposure to silver as both a critical mineral and a strategic defense metal, by advancing one of the largest undeveloped primary silver projects on U.S. soil at a time of tightening physical markets and rising geopolitical risk.

Apollo controls two advanced silver assets in tier-one jurisdictions, with its flagship Calico project located in the USA and Cinco de Mayo project in Mexico, regions with long mining histories, established infrastructure, and clear permitting frameworks. That jurisdictional profile positions the assets squarely within the emerging policy focus on secure domestic supply chains.

In 2025 Apollo, reported an updated Mineral Resource Estimate for Calico that reflected a 61% increase in tonnage and a 14% increase in contained silver ounces compared with the Company’s prior estimate. An updated NI 43-101 technical report (effective June 30, 2025) shows the Waterloo deposit, using a 47 g/t silver equivalent cut-off grade, includes 125 M oz of silver in in 55Mt at an average grade of 71 g/t silver in the Measured and Indicated categories, and 0.51 Moz silver in 0.6 Mt at an average of 26 g/t silver in the Inferred category. The Langtry Deposit now contains 57 Moz silver in 24 Mt at an average grade of 73 g/t in the Inferred category, using a 43 g/t silver cut-off grade.

In late 2025 the company announced a $25 million strategic private placement with cornerstone participation from Eric Sprott and Jupiter Asset Management, reinforcing shareholder alignment and providing capital for Calico drilling and development programs through 2026. And, on December 29 2025, company announced a $2.5 million upsizing to the financing to allow for insider participation.

✅ Final take

For investors, the combination of non-recyclable defense consumption and a 150-million-ounce annual deficit creates a compelling case for significantly higher prices.

- The $150 Scenario: While once dismissed as speculative, the prolonged structural deficit and inventory depletion have made $150 silver a plausible target for late 2026.

- Leverage: Silver typically outperforms gold in late-stage bull markets. With the gold-silver ratio compressing from 105x to levels below 70x in 2025, the “humble metal” is seeing its industrial and strategic premiums finally priced in.

In an era of sustained rearmament, silver is no longer just an industrial workhorse or a jewelry-box staple. It is a strategic asset embedded in the fabric of national defense. In fact, defense is the only major silver consumer whose usage is both price‑inelastic and largely undisclosed, making it a structural ‘surprise bid’ in every future conflict or rearmament cycle

If current rearmament and energy trends continue, the world is heading toward a market that simply cannot supply enough physical silver for every claimant.