📌 Key Takeaways

- BloombergNEF projects $2.9 trillion per year in energy transition investment over 2026–2030, up ~25% from 2025.

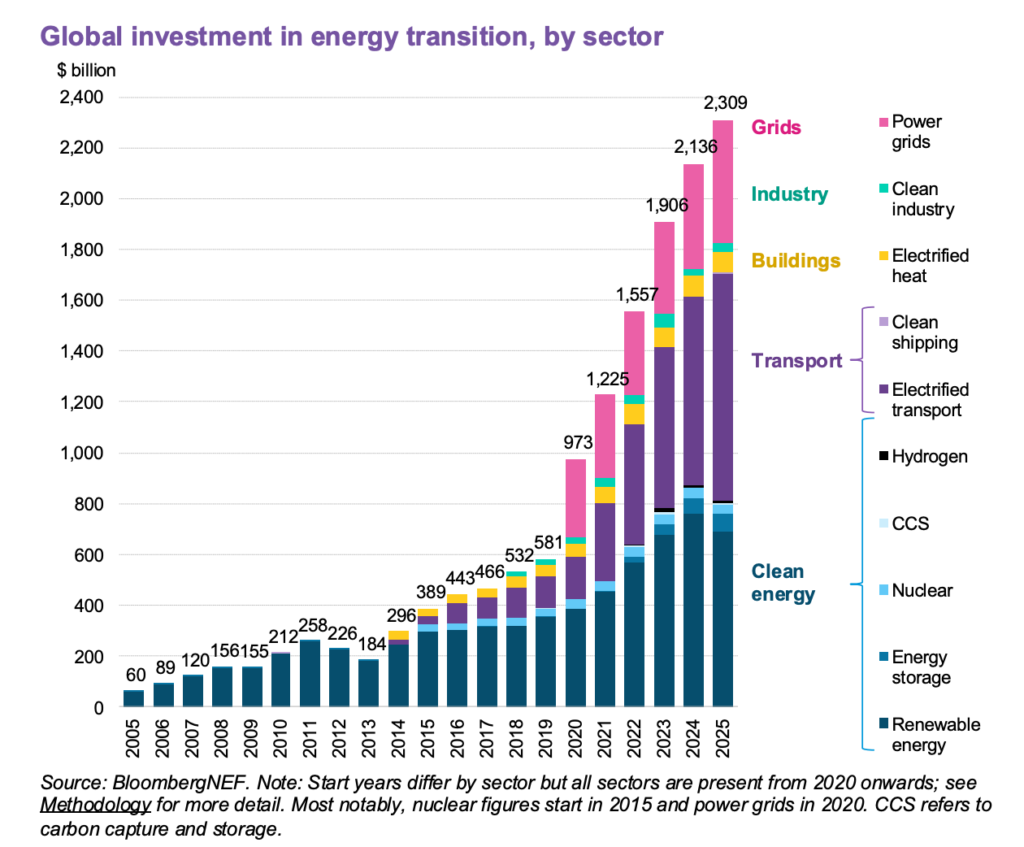

- Global energy transition investment hit a record $2.3 trillion in 2025, up 8% from a year earlier. Climate-tech equity finance returned to growth after three years of decline with a 53% jump, while energy transition debt issuance climbed to $1.2 trillion.

- Clean energy supply-chain investment reached only $127 billion in 2025, far below deployment needs.

- Lithium, nickel, and cobalt investment must accelerate to avoid cost inflation and bottlenecks.

Under BloombergNEF’s base-case outlook, global energy transition investment is set to average around $2.9 trillion per year between 2026 and 2030 — roughly 25% higher than the $2.3 trillion deployed in 2025 — underscoring the accelerating scale of capital required to electrify the global economy.

The projection follows a year in which energy transition investment hit a record $2.3 trillion, rising 8% year-on-year despite trade disruptions and geopolitical tension. BloombergNEF notes that growth has slowed from post-pandemic highs, but absolute spending continues to climb as electrification deepens across transport, power, and industry .

Where the money is going

Electrified transport absorbed $893 billion in 2025, making it the largest single component of the transition. Renewable energy followed with $690 billion, while power grid investment jumped 17% to $483 billion as utilities raced to connect new generation and manage rising demand from EVs and data centers .

Together, these three sectors accounted for more than $2 trillion of total spending — and they are among the most mineral-intensive parts of the energy transition.

- Electrified transport: $893bn

- Renewable energy: $690bn

- Power grids: $483bn

The upstream mismatch

While downstream deployment surged, clean energy supply-chain investment — including mining and processing of battery metals — reached just $127 billion in 2025, up 6% year-on-year. BloombergNEF highlights that this figure covers spending on lithium, cobalt, and nickel mines and refineries, alongside battery and clean-tech manufacturing capacity .

The imbalance is structural. Energy transition deployment represented $2.4 trillion of real-economy investment in 2025, while upstream supply chains captured a small fraction of that total. BloombergNEF warns that aligning with net-zero pathways would require significantly faster growth in lithium mining and cobalt refining, with wind manufacturing also at risk of falling short .

Costs today, pressure tomorrow

Overcapacity in clean-tech manufacturing — particularly solar — continues to push equipment prices lower. Battery manufacturing is still expanding, reinforcing short-term deflationary pressure across parts of the value chain. But BloombergNEF cautions that persistent underinvestment in raw materials risks reversing these cost declines as demand scales toward the end of the decade .

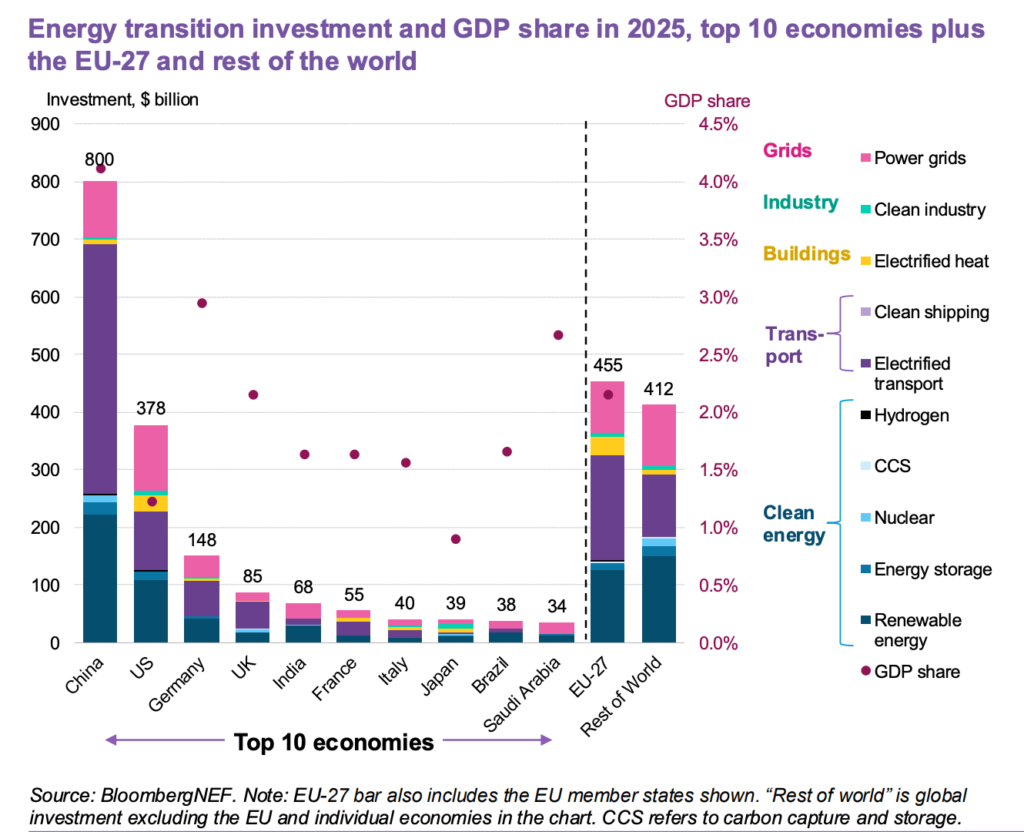

China remains the dominant hub for clean-tech manufacturing, but its share of global supply-chain investment is gradually declining as the US, EU, and India attempt to onshore production — often with higher costs and longer lead times .

Why it matters

BloombergNEF’s projection of $2.9 trillion per year through 2030 implies a sustained step-change in demand for copper, lithium, nickel, and other critical minerals. The strategic risk is no longer whether the energy transition is funded — but whether mineral supply, permitting, and processing capacity can scale fast enough to support it.

For investors and policymakers, the next phase of the transition will be defined less by technology adoption curves — and more by the hard constraints of geology, capital discipline, and geopolitics.