📌 Key Takeaways

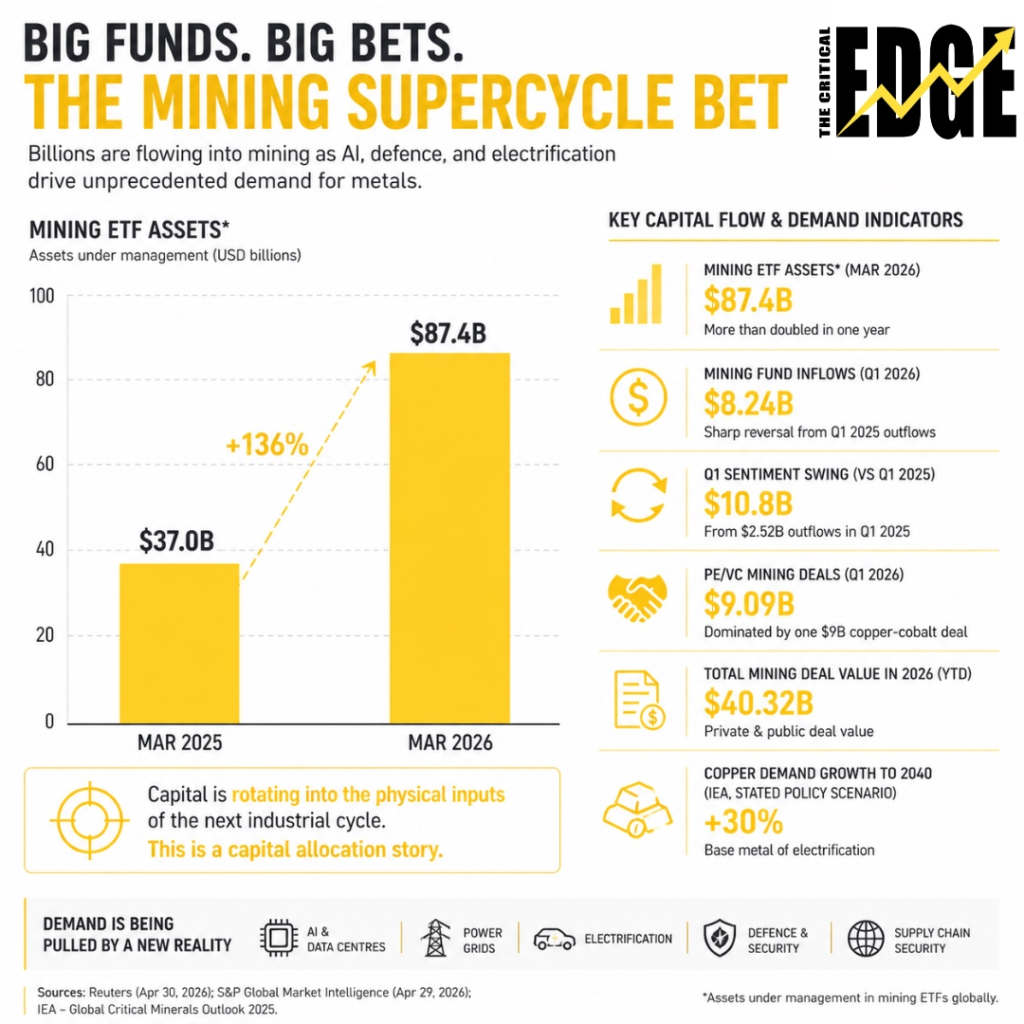

- Mining ETF assets more than doubled to $87.4 billion by March 2026, according to Reuters.

- Investors put $8.24 billion into mining in Q1 2026, a sharp reversal from outflows a year earlier.

- Private equity and venture capital mining deals hit $9.09 billion in Q1 2026, but the figure was dominated by one $9 billion copper-cobalt transaction.

- The trade is moving beyond gold into copper, aluminium, rare earths and other strategic metals.

Mining ETF assets have more than doubled in a year to $87.4 billion, as large funds rotate into metals on the view that AI infrastructure, defence spending and electrification are pushing the market toward a new mining supercycle, according to new data by Reuters.

Investors put $8.24 billion into mining in the first quarter of 2026. That marks a $10.8 billion turnaround from the first quarter of 2025, when the sector saw $2.52 billion of outflows after US tariff announcements hit sentiment.

Investors are not just buying mining because metals are cheap. They are buying miners because the physical economy is becoming more metal-intensive.

📈 Why are investors moving into mining now?

The new demand stack is broader than the China-led urbanisation boom of the 2000s.

This cycle is being pulled by power grids, data centres, electric vehicles, charging infrastructure, defence procurement and supply-chain security. The IEA expects copper demand to rise by 30% by 2040 under stated policy settings, while lithium demand rises fivefold and nickel and graphite demand double.

That matters because copper is not a niche battery metal. It is the base metal of electrification.

The IEA said lithium demand expanded by nearly 30% year on year in 2024, while long-term demand projections remain strongest for lithium, copper, nickel, graphite, cobalt and rare earths.

This is why the fund flow is moving beyond gold.

Copper funds attracted $198 million in March, while the VanEck Gold Miners ETF lost $710 million in the month, even though it remained up almost $1 billion year-to-date.

The market is treating industrial metals less like pure cyclicals and more like strategic infrastructure.

⛏️ Mining M&A is following the money

The flow into public markets is being matched by private capital, but with an important caveat.

Private equity and venture capital metals and mining deals reached $9.09 billion in the first quarter of 2026, according to S&P Global Market Intelligence. But the number was dominated by one transaction: the planned $9 billion acquisition of a 40% stake in Glencore’s Mutanda and Kamoto copper-cobalt assets in the Democratic Republic of Congo.

Total private and public metals and mining deal value has already reached $40.32 billion in 2026, according to S&P Global.

That deal tells the story.

Private capital is not just chasing price momentum. It is moving into copper, cobalt and critical minerals where governments now see supply as an industrial policy issue.

This connects directly with the broader push to create a Western premium for secure critical mineral supply.

The numbers behind the mining supercycle trade

| Indicator | Latest figure | Why it matters |

|---|---|---|

| Mining ETF assets | $87.4bn | More than doubled in one year |

| Mining fund inflows, Q1 2026 | $8.24bn | Sharp reversal from 2025 outflows |

| Q1 sentiment swing | $10.8bn | Shows speed of rotation into mining |

| PE/VC mining deals, Q1 2026 | $9.09bn | Dominated by one $9bn copper-cobalt deal |

| Total mining deal value in 2026 | $40.32bn | M&A is accelerating |

| Copper demand growth to 2040 | +30% | IEA base-case pressure on supply |

Sources: Reuters, S&P Global Market Intelligence, IEA

💰 Why does this matter for mining stocks?

The mining sector is still small compared with technology.

The top five mining companies represent just 0.4% of the MSCI ACWI Index, compared with 16.8% for the top five technology companies. Metals and mining products account for only 0.57% of total equity ETF market share.

That creates the opportunity — and the risk. If large pools of capital continue rotating into a small sector, prices can move fast. But the same small market size also means reversals can be sharp.

Reuters reported that metals futures trading volumes including copper and aluminium on the London Metal Exchange reached about $21 trillion last year. That compares with more than $85 trillion in Nasdaq-100 futures and more than $135 trillion in S&P 500 futures.

Major miners still trade at roughly 7–8 times EV/EBITDA, below the 14 times multiples seen during the 2008–2010 boom. That gives investors a simple thesis: if this is a real mining supercycle, the equities may not yet have fully priced it.

💥 What could break the trade?

The risk is not only demand. It is inflation, politics, permitting and execution.

Mining is capital-intensive, slow to permit and exposed to energy, labour and geopolitical risk. More capital into metals can lift prices, but higher metal prices also feed back into infrastructure costs, defence procurement and the energy transition.

The USGS said the value of US nonfuel mineral production rose 5.6% to $112 billion in 2025, while mineral-reliant industries represented $4.09 trillion in value, more than one-eighth of the US economy.

That is the strategic tension.

Governments want more secure supply. Investors want exposure to scarcity. Consumers and manufacturers want lower prices. They cannot all get what they want at once.

The mining supercycle trade is now pricing in the collision.

📌 Mining is becoming a capital rotation story

The mining supercycle bet is not just about copper prices.

It is about capital moving into the physical inputs of AI, defence, electrification and industrial security. Mining ETFs have doubled. Private equity is writing billion-dollar cheques. Governments are entering deals that would once have been left to commodity traders and majors.

The opportunity is clear: miners control assets the next industrial cycle needs.

The risk is just as clear: these are small, volatile markets, and the money is arriving before supply can respond. That is why the mining supercycle matters. It is no longer only a commodity story. It is a capital allocation story.