📌 Key Takeaways

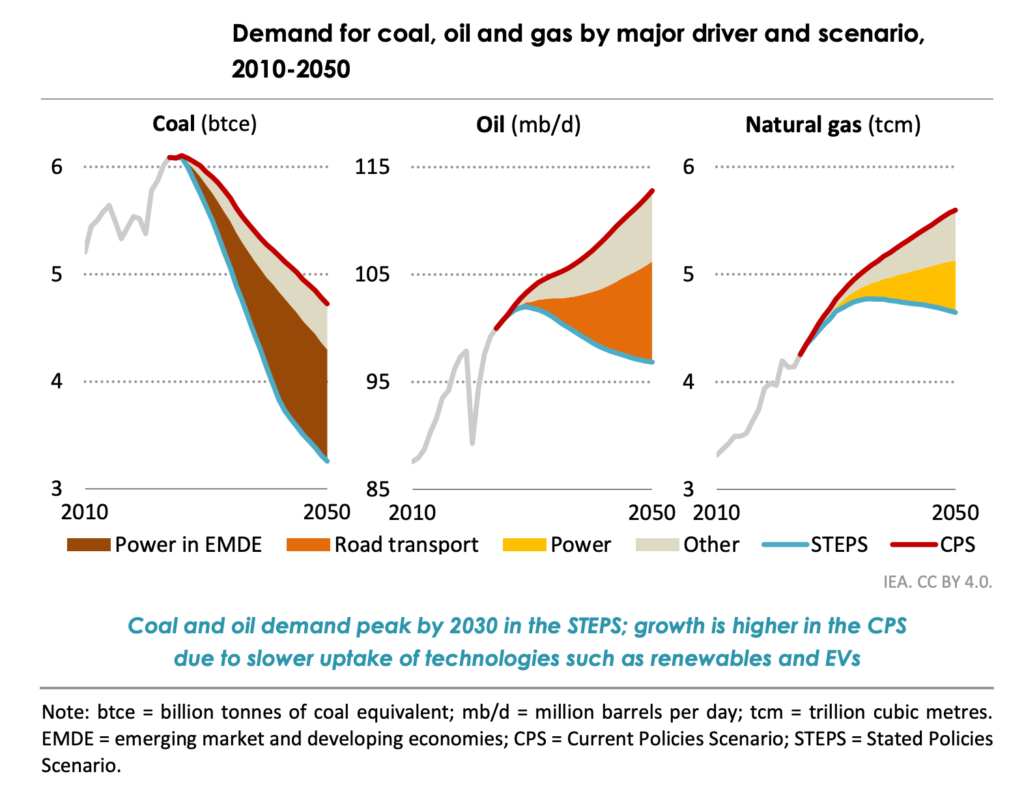

- The IEA now projects oil demand to keep rising into the 2030s, hitting 113 million barrels per day (mb/d) by 2050 under current policies.

- Even in its “Stated Policies Scenario,” demand plateaus around 2030 — not declines as earlier forecast.

- The report marks a departure from 2023 forecasts that predicted an oil peak before the decade’s end.

- The IEA states: “demand for oil and natural gas continue to grow to 2050.”

The International Energy Agency has quietly rewritten one of the most controversial storylines of the energy transition. In its World Energy Outlook 2025, the IEA concedes that global oil demand will remain robust and continue to grow to 2050, reversing its 2023 stance that consumption had entered terminal decline.

The shift is driven by revised projections for transport, petrochemicals, and emerging markets, and comes as geopolitical instability and sluggish renewables buildout reinforce oil’s strategic role.

Oil Demand: The Peak That Never Came

In previous years, the IEA predicted that global oil demand would peak by 2030. Two years later, that certainty is gone.

“In 2035, total oil demand is 5 million barrels per day (mb/d) higher in the CPS than in the STEPS, with 40% of this difference due to the slowdown in EV sales” — World Energy Outlook, IEA

In the 2025 Outlook, the IEA’s Current Policies Scenario (CPS) shows oil some 25 mb/d of new oil projects need to be approved to keep markets balanced to 2035, compared with around 20 mb/d in the STEPS. Upstream oil and gas investment needs in the Stated Policies Scenario (STEPS) out to 2035 are broadly in line with the average level of spending in recent years, around USD 100 billion more than that average is needed every year in the CPS.

That means, under realistic assumptions, oil remains central to global energy systems for another 25 years.

Why the IEA Changed Course

The agency cites four structural reasons why oil demand has defied expectations:

- Petrochemicals: Plastics, fertilizers, and industrial feedstocks now account for a growing share of oil use. Demand for these products in India, Southeast Asia, and Africa continues to surge.

- Aviation and Freight: Air travel has recovered faster than expected. Freight volumes are up 15% year-on-year in Asia, and no scalable substitutes exist.

- Slower EV Adoption: The IEA revised down electric vehicle growth projections, especially in the US, where weaker subsidies and higher rates have cooled sales.

- Emerging Market Growth: Developing economies account for nearly all oil demand growth to 2035 — led by India, the Middle East, and Latin America.

These factors collectively push back the oil demand peak well into the 2030s — if it comes at all.

A Tale of Two Markets

The IEA describes a dual-speed oil economy emerging:

- Advanced economies see flat or falling consumption.

- Developing economies — still urbanizing and industrializing — are only entering their oil-intensive phase.

This structural divergence keeps global demand resilient even as OECD nations decarbonize.

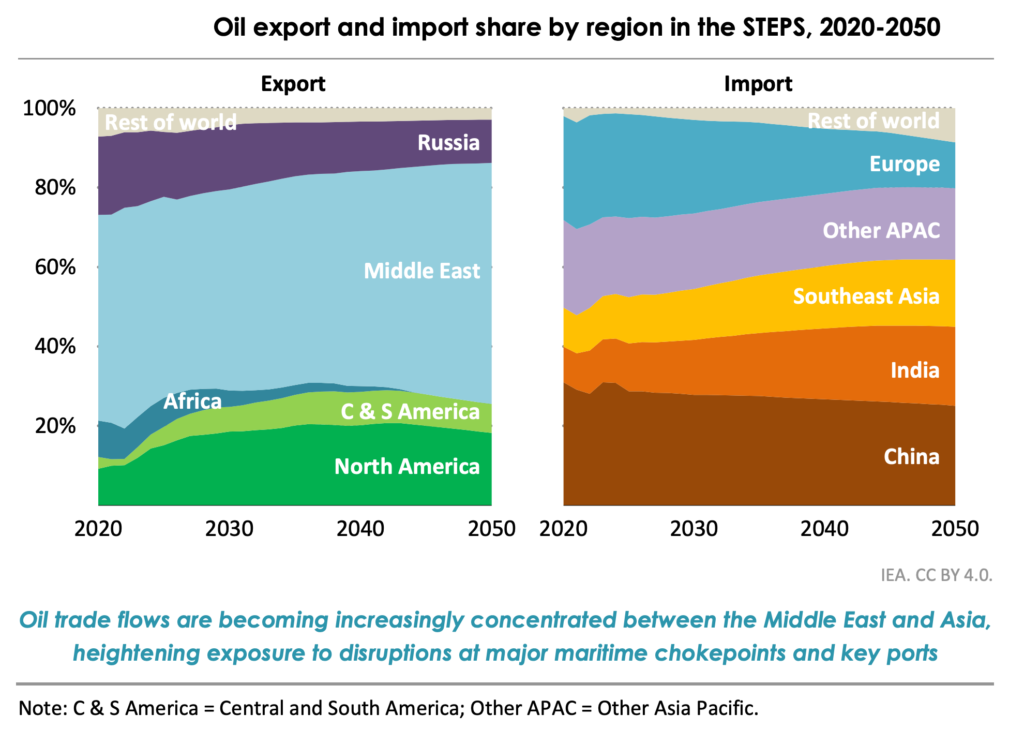

Between now and 2035, 80% of new oil demand comes from non-OECD Asia, with India alone accounting for nearly one-third of that growth.

The Investment Paradox

The IEA warns that underinvestment now risks creating volatility later.

That means massive new capital expenditure to prevent price shocks. Yet, ESG mandates and policy uncertainty have starved traditional producers of funding.

“If all capital investment in current oil and gas production were to cease immediately, global oil supply would fall by around 5.5 mb/d each year and natural gas output by 270 bcm” — World Energy Outlook 2025, IEA

The irony is clear: a rush to decarbonize without replacing oil infrastructure could trigger the very crisis the energy transition hoped to avoid.

Energy Security and the New Oil Geography

The IEA’s tone on energy security has hardened just as critical minerals and supply chains face new geopolitical risks.

A quintet of producers — the US, Canada, Brazil, Guyana, and Argentina — is expected to drive most new output growth through 2035. The IEA also notes the resurgence of Middle Eastern exports, as Gulf producers consolidate low-cost dominance amid Western underinvestment.

Investor Insight:

The IEA now sees oil’s role enduring “for decades,” with only its composition, not its relevance, changing — from fuels for cars to feedstocks for chemicals, aviation, and heavy industry.

Conclusion: The End of the Oil Decline Narrative

The IEA’s World Energy Outlook 2025 is a turning point.

Oil demand has not peaked. Nor will it soon.

As the agency itself admits, the world is entering an “Age of Electricity” — but electricity still runs on oil, gas, and the materials they power.

The age of decline, for oil at least, has been postponed.

Suggested URL: /iea-2025-oil-demand-forecast

Primary Keyword: oil demand outlook

Secondary Keywords: IEA 2025, energy transition, oil supply, energy security, peak oil forecast