📌 Key Takeaways

- The Loan Programs Office (LPO) at the Department of Energy will channel its largest-ever financing allocation into nuclear power plants.

- A recent landmark partnership between the U.S. government and Westinghouse Electric/Cameco Corporation/Brookfield Asset Management targets at least US $80 billion of reactor builds.

- Historical cost overruns remain a major risk: the latest U.S. reactor builds cost around US $35 billion, more than double initial estimates.

- The financing push is directly linked to surging demand from AI, data centers and electrification trends – nuclear is now framed as foundational infrastructure.

Nuclear power will receive the largest share of funding from the Energy Department’s loan office as the Trump administration accelerates plans to build a new fleet of reactors, Energy Secretary Chris Wright has announced.

“We have significant lending authority at the loan program office… By far the biggest use of those dollars will be for nuclear power plants — to get those first plants built” — the Secretary of Energy said at a conference hosted by the American Nuclear Society in Washington D.C.

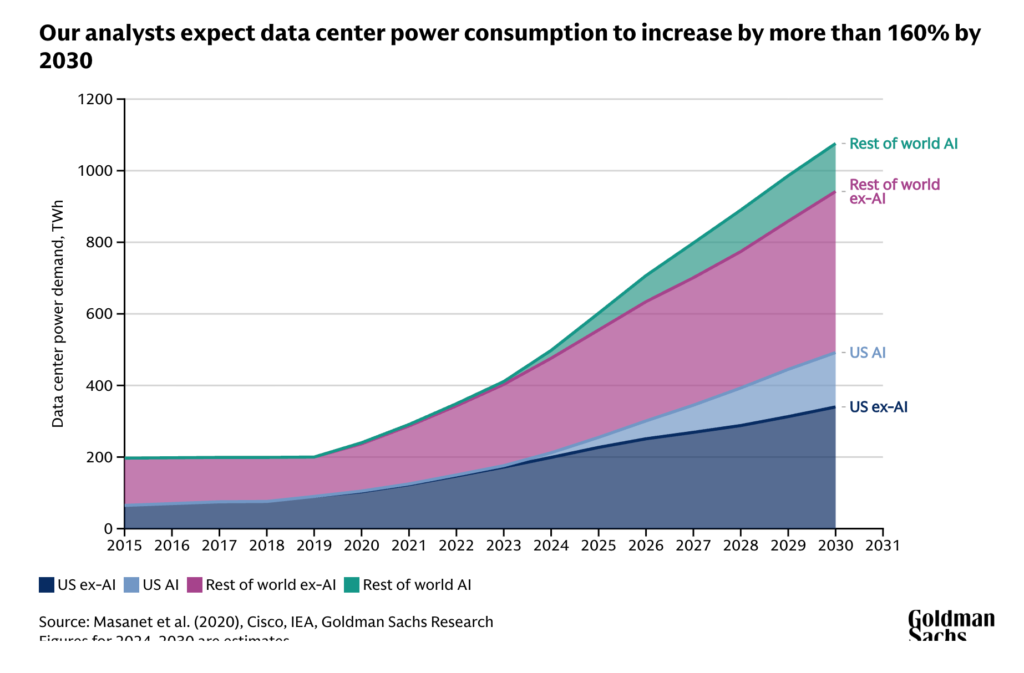

Goldman Sachs estimates 85-90 gigawatts (GW) of new nuclear capacity would be needed to meet all of the data center power demand growth expected by 2030 (relative to 2023). But well less than 10% will be available globally by 2030.

Long dormant in the U.S., large-scale nuclear new builds are suddenly re-emerging as a strategic priority as the race to build out data centers demands record amount of energy — and is sending electricity prices rising.

The rationale: with data center, AI and electric-load growth zooming, utilities and tech firms are signalling that current grid expansion cannot keep pace. Wright flagged that tech companies will bring “billions of dollars of equity capital from very creditworthy providers,” which the LPO will match “three to one, maybe even up to four to one, with low-cost debt dollars.”

The challenge is cost.

In plain terms, nuclear is being repositioned as foundational to both decarbonisation and the next wave of digital infrastructure. That has major implications for miners, reactor-equipment suppliers, developers and critical-minerals chains.

The Financing Strategy: LPO + Private Capital

The LPO has “hundreds of billions” of loan/loan-guarantee capacity and now intends to prioritise nuclear.

Here’s how the model is expected to work:

- Private investors (utilities, tech firms) commit equity.

- The LPO provides low-cost debt or guarantees — amplifying the private capital by 3–4×.

- Government also seeks profit-sharing or upside stakes in reactor build-out deals (as seen in the $80 bn programme).

This stacking of private and public capital is a shift from the clean-tech subsidy era to “industrial-scale infrastructure finance.”

Cost & Roll-Out Risk: The $35 bn Benchmark

The upside is real; the risk is also steep. Consider the U.S. benchmark: Plant Vogtle Units 3 & 4 (Georgia) cost about US $35 billion and were years behind schedule.

That sets a caution flag: even with government backing, new builds remain vulnerable to:

- Supply-chain shocks

- Labour shortages

- Regulatory/licensing delays

- Cost inflation

In other words: cost leverage works — but only if execution improves.

Further, one commentary noted that annual investment in nuclear would need to double to around US $120-billion by 2030 just to support a “rapid growth scenario”.

Deal Volume & Market Signal: $80 Billion and Counting

On 28 Oct 2025, the U.S. announced a partnership to build at least US $80 billion in nuclear reactors via Westinghouse, Cameco and Brookfield. The government will assist financing and permitting; in return it gets a 20% share of profits after $17.5 billion and potentially 20% equity if an IPO occurs by 2029.

This deal sends multiple signals:

- Nuclear is no longer niche; it is industrial scale.

- Investors should expect long-lead projects, given past execution timelines.

- Critical minerals (uranium, HALEU, nickel-steel forgings) and reactor modular supply chains are getting materially pulled in.

Conclusion

The U.S. federal government has signalled that the biggest deployment of the DOE’s Loan Programs Office financing will go into nuclear power. That comes as at least US $80 billion of reactor-build plans are announced, and as the sector faces both a boom in demand (AI/data centres) and a legacy of cost risk.

For investors, this means nuclear is no longer a fringe energy play — it’s infrastructure scale. But the risk profile remains elevated. In the mining and critical-minerals sphere, this pivot opens fresh angles: uranium production, supply-chain metals, fabrication.

The financing push aligns with the Donald Trump administration’s agenda for energy dominance and AI leadership. Reactor build-out is framed as a national-security project, not just a climate play.

The next 18-24 months will be critical: do new projects avoid the overruns of the past? Can regulatory/licensing timelines be compressed? If yes, the nuclear build-out becomes a core part of the energy-transition and investment narrative.

For critical-minerals investors (uranium, zirconium, nickel-steel forgings), the stakes just scaled up.