Key Takeaways

- DRC ends cobalt export ban on October 16, 2025, replacing it with quotas.

- Quotas: 18,125 tonnes for the rest of 2025; 96,600 tonnes annually for 2026 and 2027.

- The country produced 220,000 tonnes in 2024—over 70% of global supply. Quotas cap exports at less than half that.

- Policy aims to curb oversupply, enforce traceability, and support domestic refining.

🚫 From Ban to Quota

The Democratic Republic of Congo (DRC), which accounts for more than 70% of global cobalt supply, will end its export ban on October 16. First imposed in February 2025 as prices collapsed to nine-year lows, the ban was extended mid-year before the government opted for a new system.

Instead of halting exports outright, Congo will introduce quotas: 18,125 tonnes allowed for the remainder of 2025, and 96,600 tonnes each year in 2026 and 2027.

Allocations will be based on companies’ historical exports, with 10% of the quota reserved for “strategic national projects.” The regulator retains the right to buy back excess production or adjust quotas if market conditions or infrastructure warrant changes.

⛏️ How much cobalt does Congo produce?

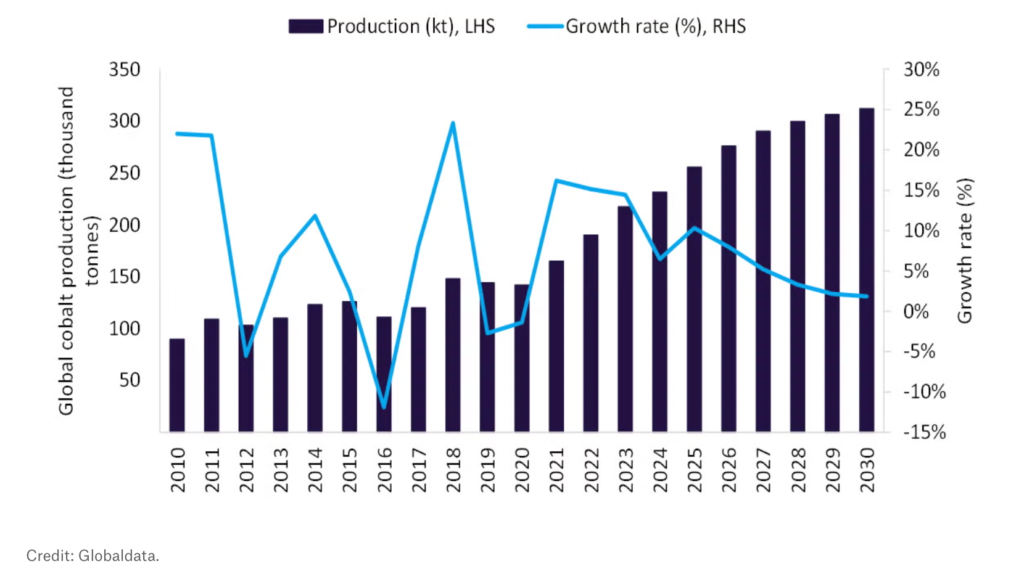

In 2024, DRC mined around 220,000 tonnes of cobalt out of global production of 290,000 tonnes, according to the USGS. That means quotas for 2026 and 2027 represent less than half of Congo’s actual output from the previous year.

The move is designed to rebalance a market struggling with oversupply: global production has surged in recent years while demand growth has lagged, driving cobalt to multi-year price lows.

Battery demand remains the long-term driver, but short-term gluts have squeezed producers. Indonesia has emerged as a fast-growing supplier, yet Congo still dominates the sector. Restricting exports through quotas is an attempt to restore price stability while forcing buyers toward more traceable, ESG-compliant supply chains.

Cobalt Market in Numbers

- Global output 2024: ~290,000 tonnes

- DRC share: ~220,000 tonnes (~76%)

- Quota 2026–27: 96,600 tonnes/year

- Gap vs 2024 output: More than 120,000 tonnes

(Source: USGS 2025)

What are the Implications: Risks and Opportunities

For buyers, the quota system signals tighter supply ahead. With exports capped well below recent output levels, cobalt prices are expected to firm, potentially sharply, as stockpiles are drawn down. Allocation rules could disadvantage smaller or newer producers, while enforcement of traceability—particularly in the artisanal sector—remains uncertain.

For investors, the opportunity lies in exposure to diversified cobalt miners or refiners outside DRC, which could benefit from price upside. Companies able to prove supply chain integrity will command premiums, and downstream manufacturers will look to lock in long-term contracts. On the policy side, the quota system pushes for in-country refining and processing, likely attracting investment into Congolese projects aligned with “strategic” designations.

The risk, however, is geopolitical. DRC’s ability to enforce quotas, curb illegal mining, and maintain stability in mining regions is far from assured. Regulatory shifts could arrive quickly, and companies heavily exposed to Congolese cobalt remain vulnerable.

Is the Cobalt Market headed Towards Deficit by 2026?

Analysts expect the cobalt market to move from surplus to deficit by 2026. Restrained exports from Congo coincide with accelerating demand from the EV sector, where cobalt remains critical for many cathode chemistries. USGS warns that much of the world’s prospective new cobalt capacity is still in early stages—dependent on financing, permitting, and infrastructure. Even with Indonesia scaling up, global supply growth may not keep pace with demand once quotas tighten.

📌 Why It Matters

Congo’s shift from an outright ban to strict quotas reshapes the global cobalt market. For investors, it suggests upside risk for prices and a premium on traceable, diversified supply. For policymakers, it underlines the strategic vulnerability of relying on a single jurisdiction for more than two-thirds of a mineral critical to the energy transition. The cobalt balance is likely to move into deficit by 2026, setting the stage for heightened competition over supply contracts and new urgency in diversification efforts.