📌 Key Takeaways

- The U.S. federal government is preparing to acquire and own up to 10 large nuclear reactors, financed via a US$550 billion investment commitment made by Japan.

- Embedded in that Japanese commitment is up to US$80 billion earmarked for new reactor builds by Westinghouse Electric Co..

- This move signals a strategic shift: nuclear power is being framed as part of U.S. national-security and critical-infrastructure strategy—which carries major implications for uranium, enrichment, reactor-component supply chains and critical minerals.

The U.S. plans to own up to 10 nuclear reactors leveraging a funding pledge of US$550 billion by Japan that was signed in October 2025 to expand America’s industrial base. This will include US$80 billion for Westinghouse built reactors.

- Japan’s investment pledge: US$550 billion, non-binding.

- Funding earmark for reactor builds: Up to US$80 billion in support of Westinghouse-led projects.

- Reactor acquisition target: U.S. government plans to own as many as 10 large reactors.

Japan’s October 2025 non-binding pledge of US$550 billion in U.S.-based projects provides the financial scale and flexibility. It remains unclear whether the reactors will be existing plants or new builds, though the Westinghouse tie-in suggests toward new construction.

“The role of having the government involved in private markets is sacrosanct — you just don’t do it… But this is a national emergency,” said Carl Coe, the US Energy Department’s chief of staf at an energy conference hosted by the Tennessee Advanced Energy Business Council.

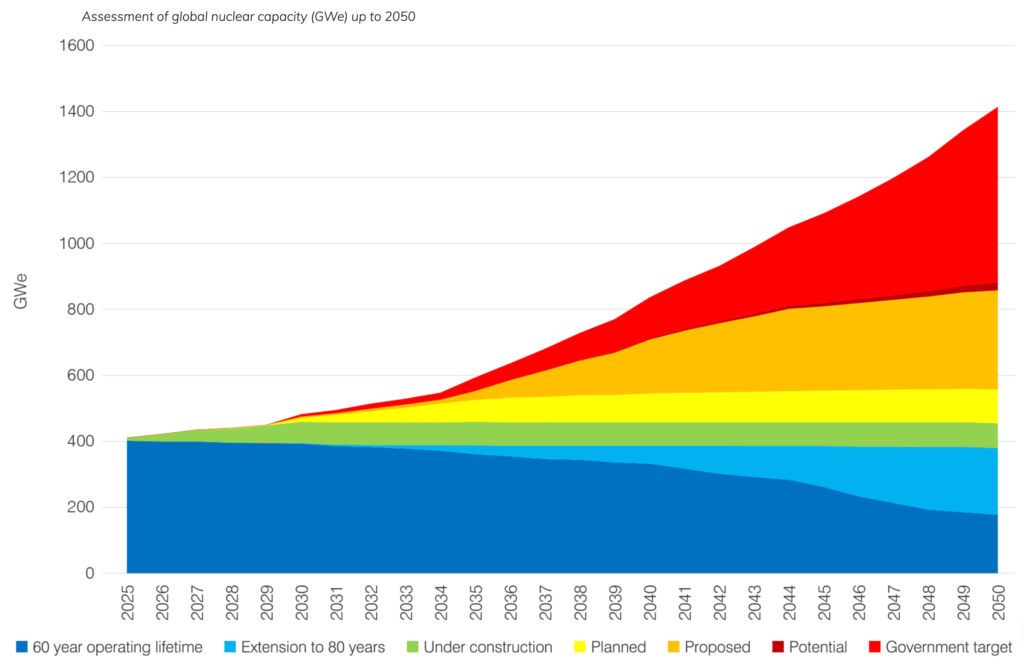

Global Nuclear Capacity and Uranium demand to Triple

The investment comes as global nuclear capacity is forecast by the World Nuclear Association (WNA) to reach 1428 GWe by 2050. This will mean global reactor requirements for uranium in 2025 are estimated at about 68,920 tU. In the WNA’s Reference Scenario these are expected to rise to just over 150,000 tU in 2040, with requirements rising to over 204,000 tU in the Upper Scenario and over 107,000 tU in the Lower Scenario by the same date.

Strategic Implications for Energy Transition & Critical Minerals

This deal moves beyond power generation: it intersects with supply-chains, materials and geopolitics.

First, nuclear is elevated as a backbone of clean energy and grid stability—alongside renewables. That means uranium mining, enrichment, and heavy reactor-component manufacturing regain strategic importance.

Second, supply-chains for components such as high-grade steel, zirconium alloys, large forgings and critical minerals (for example rare-earth or uranium by-products) gain fresh relevance. For mining and processing firms, this deal signals a direction—not just raw commodity demand, but integrated manufacturing and strategic positioning.

Third, the U.S.–Japan axis underscores the strategic overlay: Japan’s capital is being used to strengthen U.S. infrastructure, tying together industrial policy, energy transition and allied supply-chain security. Investors in critical-minerals should watch how the U.S. prioritises domestic or allied extraction/processing versus reliance on adversarial states.

🔭 What to Watch Next

Key signals for investors and policymakers:

- When will contracts be finalised? The transition from pledge to binding agreement matters.

- Which reactor technology and build sites will be selected? Will these be large reactors or small modular reactors?

- How will the supply-chain evolve for uranium mining, processing, and high-tech reactor components?

- What cost and timeline targets will the U.S. government set, and how will they compare to global benchmarks?

- How will regulatory frameworks adapt—especially permitting, licensing and financing of new nuclear plants?

Conclusion

The U.S. plan to own up to 10 nuclear reactors using funds tied to Japan’s US$550 billion commitment marks a strategic inflection. This is not a small policy tweak — it signals a firm commitment by the US in nuclear’s return as a core pillar of energy transition and industrial strategy.