📌 Key Takeaways

- The U.S. is mounting new sanctions targeting Russian oil supply, raising global oil price risks

- Chris Wright flagged U.S. moves to refill the Strategic Petroleum Reserve (SPR) as a “good time to buy” oil, underpinning upside momentum

- A tightening market, driven by supply fears and strategic shifts, places upstream oil assets and service‑exposed names in focus for investors.

The U.S. has announced new sanctions targeting Russian oil exports — aiming at tankers, refining chains and end‑buyers — as a result of Russia’s lack of serious commitment to a peace process to end the war in Ukraine.

The new US Treasury sanctions target Russia’s two largest oil companies, Open Joint Stock Company Rosneft Oil Company (Rosneft) and Lukoil OAO (Lukoil), which are now designated.

Scott Bessent, US Treasury Secretary, has encouraged allies, particularly in Europe, to join the sanctions.

“Now is the time to stop the killing and for an immediate ceasefire,” said Secretary of the Treasury Scott Bessent. “Given President Putin’s refusal to end this senseless war, Treasury is sanctioning Russia’s two largest oil companies that fund the Kremlin’s war machine. Treasury is prepared to take further action if necessary to support President Trump’s effort to end yet another war. We encourage our allies to join us in and adhere to these sanctions.”

US President Trump has also repeated his claim India has agreed to reduce oil purchases from Russia.

Strategic Buying

While sanctions reduce supply risk, the U.S. is simultaneously acting to secure its own resource base. The Department of Energy is looking to buy 1 million barrels of oil for the SPR—an early signal of U.S. energy policy reversal from draw‑down to refill.

Energy Secretary Wright described this action as “an important step in strengthening our energy security and reversing the costly … policies of the last administration.”

This matters because SPR purchases absorb barrels that might otherwise flow freely into commercial inventories or support exports—imposing added scarcity in the global market.

Why it matters for market structure

- SPR refill introduces government demand against a tightening supply backdrop—reducing slack in global markets.

- With sanctions limiting Russian crude access, U.S. citizens pay indirectly via higher global benchmarks and energy cost inflation.

- Investors often underweight the structural element of strategic stockpile policy; today’s actions hint at longer‑term implications.

Other Price Drivers: Supply Constraints, OPEC+, and Global Demand

OPEC+ and spare‑capacity limits

Beyond Russia, OPEC+ producers continue to show constrained spare capacity. With major producers already near maximum sustainable output, any disruption elsewhere can ripple quickly. In July 2025, analysts warned that OPEC could struggle to replace just a 2 m b/d Russian shortfall.

Demand‑side strength

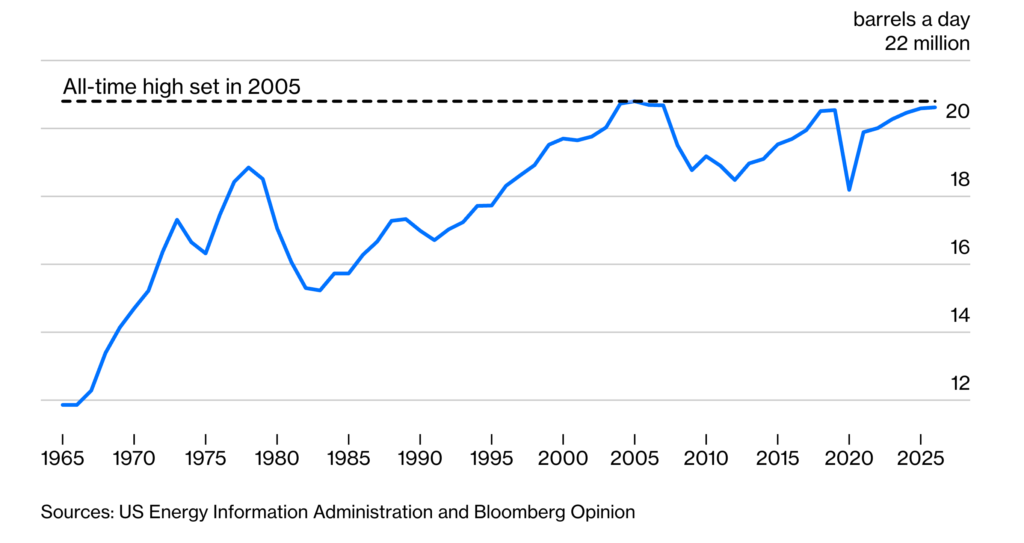

Despite global economic headwinds, oil demand is resilient, especially in Asia. Growth in shipping, petrochemicals and logistic networks supports demand above pre‑pandemic norms. Inventory draws are re‑emerging in key markets. And, in the US, oil demand is set to rise in 2025 to a 18-year high, and further increases can put American petroleum consumption above the 2005 all-time high.

Supply chain disruptions persist

Sanctions enforcement remains imperfect; Russia’s “shadow fleet” of tankers and dark‑shipping routes continue to blur official flows. Each disruption raises trading costs and adds supply‑side premium.

Wright’s public commentary signals one thing: the U.S. considers oil and gas exports and strategic reserves as tools of geopolitics and economic policy.

When a key government official states it is a “good time to buy” oil (via SPR refill announcement and sanctions signalling), it acts as a market‑anchor for risk becoming a reward.

Risks & Mitigants

- Demand shock: A sudden global economic downturn could pull demand lower, offsetting supply risks.

- Sanctions fatigue or evasion: Russia and other producers may find work‑arounds, reducing scarcity.

- Alternative supply ramps: U.S., Middle East or African producers could fill the gap faster than expected.

- Inventory glut: A hidden stock‑build in offshore inventories could delay the upward cycle.

Conclusion

The convergence of new sanctions on Russian oil, U.S. SPR refill policy, and structural supply constraints signals a re‑emergence of price upside in oil markets. The era of cheap, abundant crude may be ending. For investors, positioning now in companies leveraged to higher oil prices and supply tightness offers asymmetric upside. The risk premium is back—this time with policy backing.