📌 Key Takeaways

- The MSCI Metals & Mining Index has surged nearly 90% since early 2025, outperforming tech and financial sectors amid rising metals demand.

- AI infrastructure, robotics, EVs, and electrification are driving structural demand growth for copper, aluminium, and critical minerals.

- Copper demand could rise 50% by 2040, with supply deficits emerging without new mining investment.

- Despite the rally, mining equities still trade at valuation discounts versus historical norms, suggesting room for re-rating.

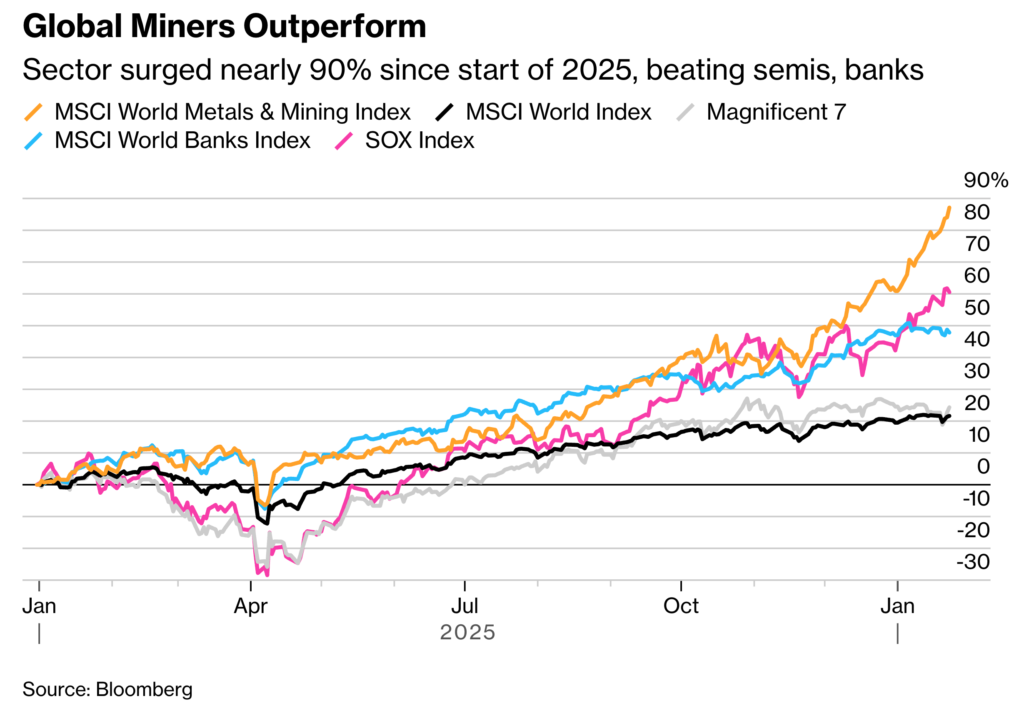

📈 Mining stocks are outperforming — but the story may only be starting

Mining equities have become one of the best-performing asset classes of the past year. The MSCI Metals and Mining Index has gained nearly 90% since early 2025, beating sectors from semiconductors to global banks as investors rotate toward real assets leveraged to the industrial cycle.

The catalyst is structural rather than cyclical. Analysts increasingly link the sector’s re-rating to a convergence of demand drivers — AI infrastructure, robotics, electric vehicles, and energy transition investments — all of which require significant volumes of metals.

Unlike previous commodity rallies driven primarily by China’s construction cycle, the current move is anchored in technology and infrastructure build-outs that require physical inputs at scale. AI may be digital, but its supply chain is deeply material.

🤖 Why AI could trigger a mining supercycle

The emerging investment thesis is straightforward: AI growth is materially intensive.

AI data centers require substantial copper for power transmission, cooling systems, and connectivity infrastructure. Estimates suggest AI-focused data centers use roughly double the copper of conventional facilities.

At the macro level, S&P Global forecasts global copper demand could rise by 50% by 2040, driven by AI, defense technologies, electrification, and robotics.

Even short-term data reflects this acceleration. Data center copper consumption alone could reach about 740,000 tonnes in 2026, potentially approaching 1 million tonnes shortly after as AI infrastructure expands.

The implication is clear: AI is shifting from a software-led narrative toward a hardware and infrastructure story — and mining companies sit at the start of that value chain.

♻︎ Supply constraints: the other side of the supercycle equation

Supercycles require tight supply, and the mining industry enters this period after years of underinvestment.

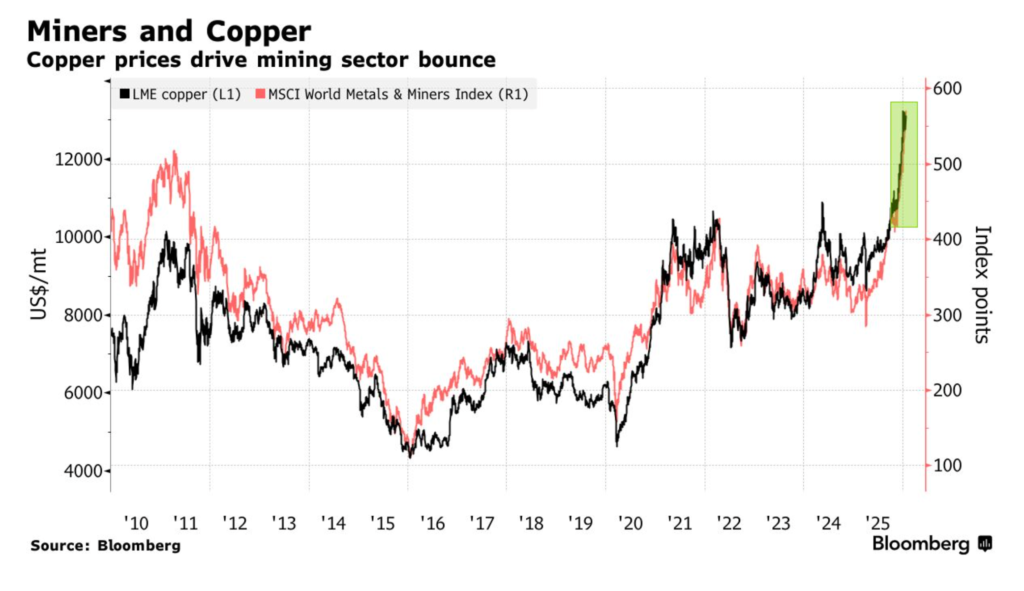

Major new mines typically take more than a decade from discovery to production, limiting rapid supply response. At the same time, disruptions in producing regions and declining ore grades are tightening inventories. Analysts now forecast copper deficits and rising price averages, with projections approaching $11,975 per tonne in 2026 following recent highs above $14,000.

This imbalance is structural rather than temporary. Mining investment lagged during the 2010s commodity downturn, leaving insufficient pipeline capacity to meet future demand growth.

💰 Valuations remain supportive despite strong performance

Perhaps the most notable feature of the current rally is that mining equities remain relatively cheap.

Even after recent gains, some sector benchmarks still trade at roughly a 20% discount to long-term valuation multiples, suggesting investors have not fully priced in the structural shift underway.

This contrasts with previous cycles where mining stocks became crowded trades late in the rally. Today, global portfolio allocation to commodities and mining remains historically low, implying significant potential capital rotation if the supercycle narrative strengthens.

🪙 Which metals are driving investor positioning?

Not all commodities are equal in the current cycle.

Analysts increasingly favor metals linked to electrification and technology infrastructure:

| Metal | Key Demand Drivers | Outlook Signals |

|---|---|---|

| Copper | AI data centers, grids, EVs | Supply deficits, rising forecasts |

| Aluminium | Electrification, lightweighting | Production caps and supply tightness |

| Tin | Electronics and semiconductors | Strong demand outlook |

| Nickel | Batteries but oversupply risks | More muted outlook |

The divergence highlights a shift from broad commodity rallies toward selective structural winners.

💥 Risks: why this may not be a straight-line supercycle

While the narrative is compelling, several risks remain.

First, commodity markets rarely move in straight lines. Analysts warn that speculative rallies can overshoot fundamentals, leading to volatility and corrections even during longer-term uptrends.

Second, technological shifts could alter demand intensity. Changes in battery chemistry, material substitution, or AI efficiency improvements may reduce per-unit metals consumption over time.

Finally, geopolitical tensions — particularly around processing dominance and resource nationalism — could both support prices and increase operational risk.

⛏️ Conclusion: A structural shift is reshaping mining equities

Mining stocks are no longer just a cyclical trade tied to global GDP growth. The combination of AI infrastructure, electrification, and supply constraints is creating a structural demand regime that could support a prolonged re-rating.

With sector performance already strong yet valuations still discounted relative to history, the investment case increasingly centers on scarcity and strategic importance rather than pure commodity momentum.

If the current trajectory continues, mining equities may be transitioning from a late-cycle allocation into a core strategic asset — potentially marking the early stages of a new supercycle.