📌 Key Takeaways

- Market Reset: The January 2026 silver “crash” from $121/oz to the $75–$80 range has flushed out speculative froth, restoring a valuation floor based on physical industrial demand.

- Strategic Deficit: Global silver markets are in their fifth consecutive year of structural deficit, with 2025 shortfalls estimated at 215.3 million ounces.

- M&A Signal: Institutional “trust” is returning to the sector, evidenced by over US$2.5 billion in recent Mexico silver deals.

- Industrial Backbone: Solar PV, EVs, and AI data centers now account for nearly two-thirds of total silver consumption.

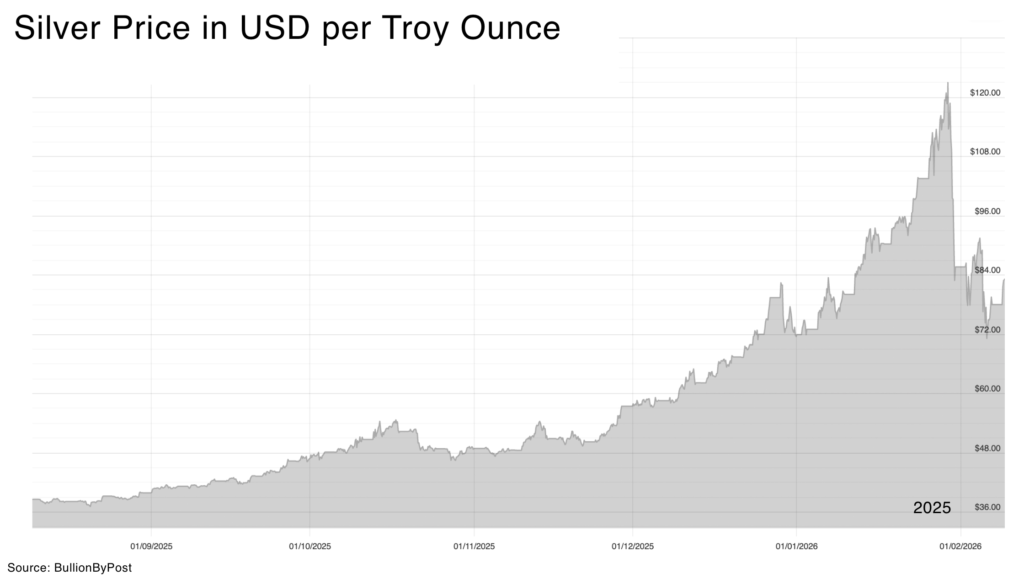

On January 30, 2026, the global silver market experienced a “liquidity wipeout” that erased nearly 37% of the metal’s value in a single trading session. Spot silver collapsed from a record peak of $121 to an intraday low of $84 per ounce, marking one of the steepest one-day percentages drop in modern commodity history.

The sell-off, catalyzed by a sudden shift in U.S. monetary policy expectations following the nomination of Kevin Warsh as the next Fed Chair, has effectively flushed out a significant amount speculative leverage, and replaced it with a fundamental entry point for long-term investors: silver mining stocks.

This environment highlights a notable valuation gap: silver mining equities, which have significantly lagged the metal’s multi-year rally, now trade at substantial discounts relative to a silver price that continues to generate historic free cash flow for producers.

The “crash” in silver prices is not a sign of weakness, but a return to reality — and strength. At $120/oz, trust in the price was non-existent. At current levels, silver mining stocks are finally trading against tangible fundamentals rather than speculative mania.

While short-term volatility is likely to persist in the silver price as the market searches for a new equilibrium. The speculative froth will ease, but the structural 215.3 million ounce deficit remains a fixed reality.

📊 The “Non-Parabolic” Trend: Where should silver be?

Investors must separate the “blow-off top” from the underlying trend. In early 2025, silver was trading at approximately $29/oz. By June 2025, it had reached a steady $37/oz, driven by solar and electronics demand.

A technical analysis of the long-term trend line — stripping away the January 2026 spike — suggests a fundamental fair value trajectory currently sitting between $55 and $65 per ounce. For example, before the parabolic move, major banks like UBS and Bank of America were already targeting $55–$65 for 2026.

Historic Silver Demand

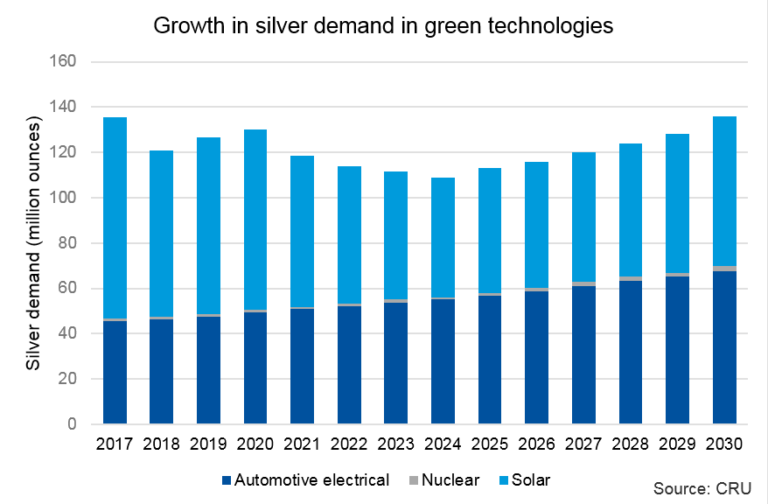

Silver’s dual role as a precious and industrial metal has never been more pronounced. Industrial fabrication hit a record in 2024 and surpassed 710 million ounces in 2025, establishing a consumption floor, just as the debasement trade introduces significant volatility into safe haven precious metals.

(see our article on “Silver Price Outlook 2026: Record Rally Amid Supply Deficit and Demand Boom“)

☀️ Solar: The 700GW Foundation

The solar industry now consumes 29% of global industrial silver, up from just 11% a decade ago. While manufacturers have “thrifted” the amount of silver per cell, the shift to high-efficiency N-type (TOPCon and HJT) cells has actually increased silver loading by 30-80% compared to older PERC models.

- Scale: The EU alone is targeting over 700GW of installed capacity by 2030, requiring a persistent, multi-decade supply of physical metal.

- Inelasticity: There is no viable substitute for silver’s conductivity in high-efficiency photovoltaics

At current installation rates, solar demand alone could consume over 250 million ounces annually by 2030 as solar installations are projected to reach 500 gigawatts each year.

⚡ Electrification: The EV & Grid Surge

The transition to electric transport has nearly doubled the silver requirement per vehicle. An average Battery Electric Vehicle (BEV) contains 25–50 grams of silver, roughly 70% more than traditional internal combustion engine (ICE) cars.

- Critical Circuits: Silver is essential for battery management systems, power electronics, and autonomous driving sensors.

- Grid Infrastructure: Upgrading global power grids to handle EV loads and renewable inputs is projected to contribute an additional 15–20 million ounces of demand in 2026 alone.

🤖 AI & Data Centers: The Digital Backbone

The explosion in Generative AI has turned data centers into a “sticky” demand pocket. Global IT power capacity has increased 53-fold since 2000, reaching nearly 50GW in 2025.

- Hardware Performance: Each new generation of AI servers requires high-performance connectors, switches, and silver-coated conductor tracks to manage massive data throughput with minimal heat loss.

“Even in the absence of precise silver-loading data, the link is clear: a 5,252% increase in IT power demand translates into more computing hardware and, consequently, greater demand for silver” — The Silver Institute, Silver Demand Forecast to Expand Across Key Technology Sectors

🚀 Defense & National Security

In late 2025, the U.S. Geological Survey (USGS) officially added silver to the Critical Minerals List. As well as critical electrification infrastructure, this reclassification acknowledges silver’s irreplaceable role in:

- Guidance Systems: Precision circuitry in missiles and satellites.

- Communications: Secure, high-frequency military-grade electronics.

- Supply Risk: With the U.S. importing over 70% of its silver, domestic primary assets are now being prioritized under national security mandates.

⛏️ Why Buy Silver Mining Stocks Now?

While the silver price has corrected, the margins for silver mining stocks remain at historic highs. Most primary silver miners have an all-in sustaining cost (AISC) between $18 and $24/oz. With silver holding in a $60–$80 range, creating a massive disconnect between extraction costs and even the most conservative market prices. This margin expansion is beginning to show up in the balance sheets of the industry’s largest players:

- Hecla Mining (HL): The largest U.S. producer reported an AISC of $11.01/oz at its primary operations in late 2025, after byproduct credits. By January 2026, Hecla achieved record quarterly revenue of $409.5 million, a 35% increase fueled by these high margins.

- Pan American Silver (PAAS): Following the integration of the high-grade Juanicipio mine, Pan American lowered its silver segment AISC guidance to $15.75–$18.25/oz for 2026. This cost discipline allowed the company to generate record attributable free cash flow of $251.7 million in a single quarter of late 2025.

- First Majestic Silver (AG): The Company reports cost guidance to reflect cash costs and all-in sustaining costs (“AISC”) on total operations at $18.17 – $19.35 on a per AgEq attributable payable ounce.

The Takeaway: The “miner trade” has shifted from a play on rising prices to a play on massive cash accumulation. At $80 silver and a $20 AISC, a miner earns roughly $60/oz or about a 75% operating margin, meaning profits are roughly three times its cost base ‚ a profile typically reserved for software companies.

| Metric | 2024 (Actual) | 2025 (Projected) | 2026 (Trend) |

| Global Mine Production | 819 Moz | 813 Moz | Stagnant |

| Industrial Demand | 680 Moz | 711 Moz | Growing |

| Total Market Deficit | -146 Moz | -215 Moz | Deepening |

| Sources: Silver Institute, Goldman Sachs |

💥 Risk still matters

This is not a straight-line trade.

A variety of major analysts forecat silver prices will continue to rise, for example, Citigroup forecasts silver will reach $150 in 2026, driven by relentless Chinese buying and dollar weakness to four-year lows.

Silver remains (very) volatile, sensitive to real rates, dollar moves, and macro liquidity. Cost pressures, including energy, labor, reagents, still threaten margins. Political risk in key mining jurisdictions remains elevated.

But those risks were present before the rally, and before the recent crash.

What has changed is trust. Markets now have a price that can be underwritten by fundamentals rather than momentum alone.