📌 Key Takeaways

- Chinese lending across Africa has fallen to its lowest level in nearly two decades, tightening capital for mining and infrastructure projects.

- Beijing’s retreat is forcing African governments and miners to seek Western, Gulf, and private capital — often at higher cost.

- The shift raises near-term financing risk for metals supply but may reshape ownership, governance, and project economics longer term.

A sharp slowdown in Chinese capital to Africa

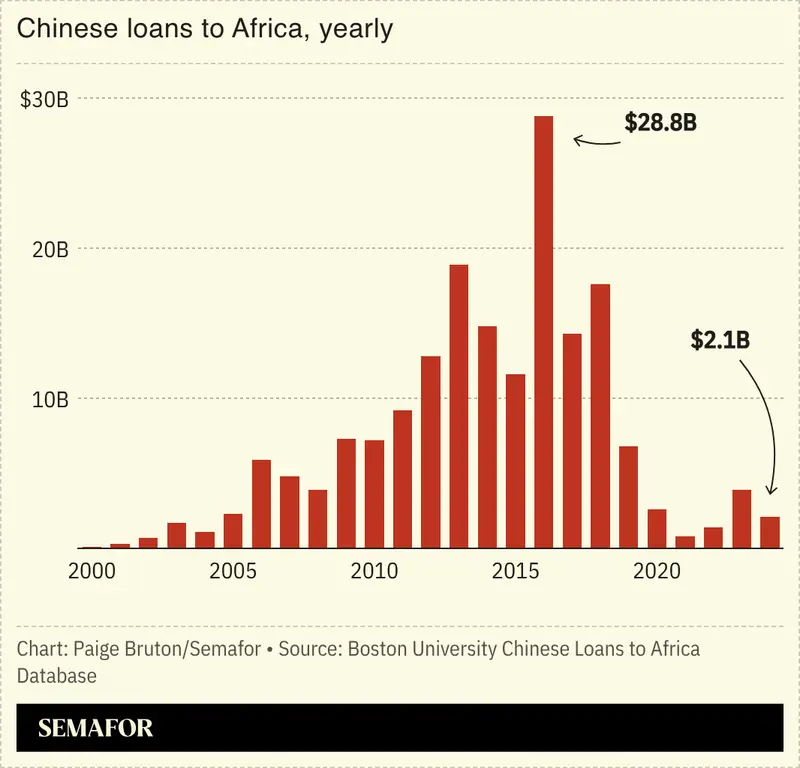

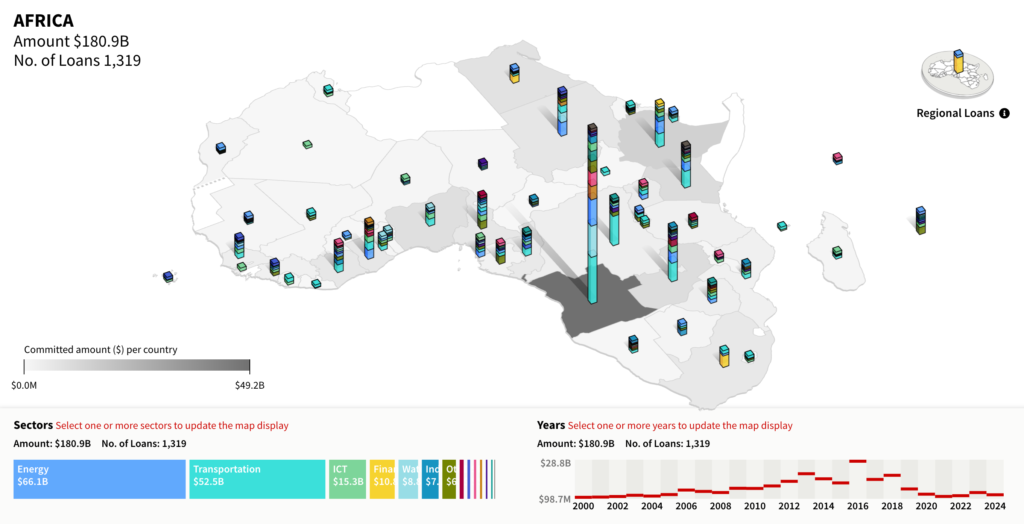

Chinese lending to Africa has entered a new phase of retrenchment. Total loan commitments from Chinese policy banks and state lenders fell to $4.6 billion in 2023, down more than 95% from the 2016 peak of roughly $75 billion, according to data from the Global Development Policy Center‘s Chinese Loans to Africa Database.

The pullback extends a multi-year decline driven by rising debt stress across the continent, weaker Chinese domestic growth, and Beijing’s shift away from large, sovereign-backed infrastructure finance.

The slowdown is now structural. Several African borrowers have entered debt restructuring talks or defaulted, pushing China to prioritise repayment, risk reduction, and smaller, commercially viable deals rather than headline Belt and Road projects, according to a report by Semafor.

What does this mean for mining?

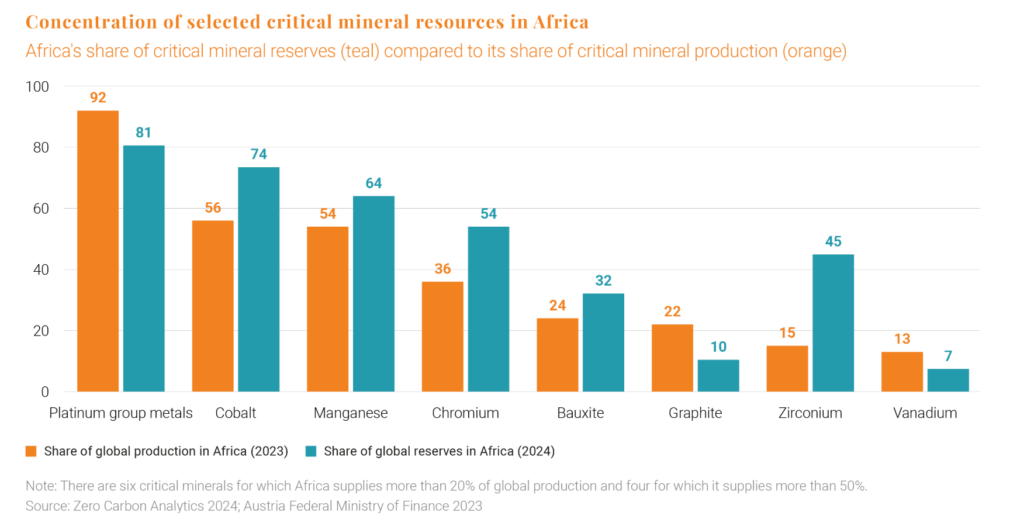

Mining and metals sit at the centre of the impact. Over the past decade, Chinese capital financed railways, ports, power, and processing capacity critical to African copper, cobalt, iron ore, bauxite, and lithium supply chains. As lending contracts, new mine developments face tighter funding conditions, longer timelines, and higher cost of capital.

This matters because Africa accounts for:

- 70% of global cobalt production

- over 20% of mined copper growth since 2015

- and an expanding share of future lithium and graphite supply

Infrastructure delays translate directly into slower supply growth — a risk as global demand for energy-transition metals accelerates.

Who fills the gap?

The retreat does not mean China is exiting African mining. Instead, it is narrowing its exposure. Chinese firms are increasingly focusing on equity stakes, offtake agreements, and brownfield expansions, shifting risk onto project partners rather than sovereign balance sheets.

At the same time, Western development banks, Gulf sovereign funds, and private capital are selectively stepping in — often demanding stricter governance, ESG compliance, and higher returns. That reshapes project economics and ownership structures, particularly in copper, lithium, and battery-linked minerals.

The strategic backdrop

For policymakers, the change cuts both ways. Reduced Chinese lending eases debt-dependency risks but exposes a financing gap just as Africa’s minerals become more strategically important to the US and Europe. For investors, the story is less about China leaving Africa — and more about who controls, finances, and prices the next wave of African metals supply.

In a market already sensitive to supply disruptions, China’s pullback adds friction at precisely the wrong moment.