📌 Key Takeaways

- The U.S. canceled a $500 million Pentagon-backed cobalt tender due to lack of supply and bidding gaps, exposing structural Western dependence on China

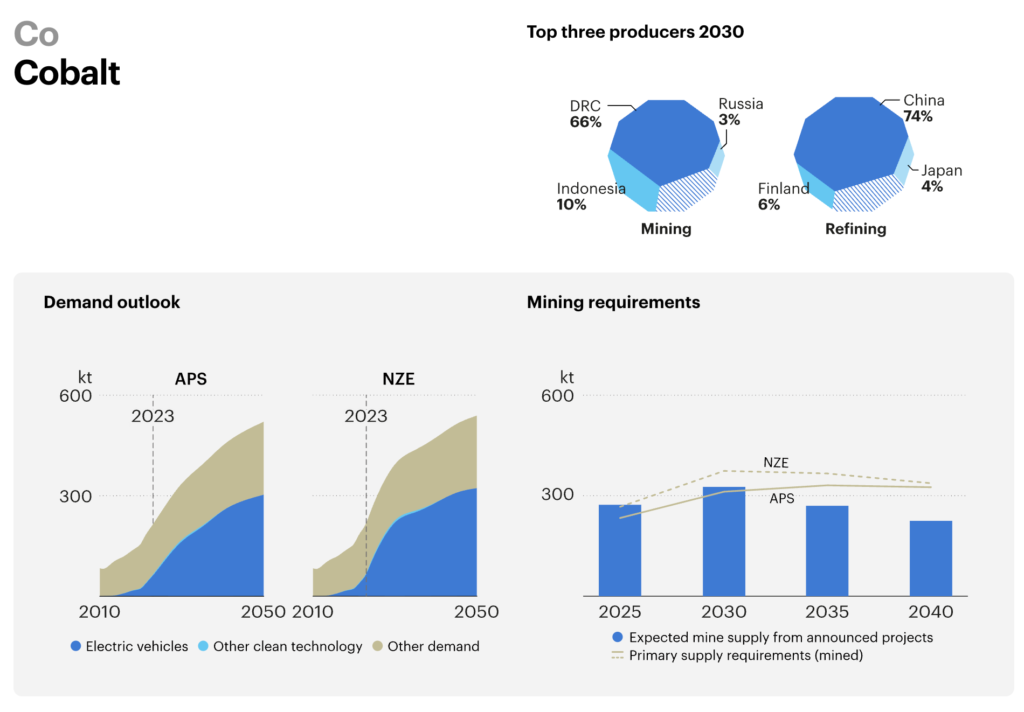

- 70% of global cobalt supply comes from the DRC and over 75% of refining is controlled by China

- The cancellation undermines Washington’s $1 billion critical minerals stockpile plan

- Signals tightening market ahead of EV and defense demand; bullish long-term for cobalt miners and refiners

The Pentagon canceled a $500 million cobalt purchase tender after failing to secure compliant bids. The tender was part of a broader U.S. push to stockpile strategic metals under the Defense Production Act to reduce dependence on China. Instead, the collapse of the initiative has exposed weaknesses in U.S. procurement strategy and the fragility of Western cobalt supply.

The move comes after reports Washington is racing to build a $1 billion strategic stockpile of critical minerals including cobalt, lithium, nickel, graphite, and rare earths to counter China’s leverage in supply chains. The cobalt tender was meant to be a cornerstone of that strategy — and this is now a serious setback.

Why cobalt matters: EVs and missiles run on it

Cobalt isn’t just a battery metal — it is a technology choke point. The U.S. Department of Energy classifies cobalt as a critical material at high risk of supply disruption because it is essential to both electric vehicle batteries and defense systems — including jet engines, missile guidance systems, and high-temperature alloys used by the U.S. military.

Global demand is set to rise from 196,000 tonnes in 2023 to 230,000 tonnes by 2030 driven by EVs, according to the IEA. Despite battery chemistry trends shifting toward lower-cobalt cathodes like LFP, cobalt remains required in high-performance NMC cathodes used for range and cold-weather stability — a priority in Western EV markets.

Cobalt Market Snapshot

- Price (metal): ~$15/lb (LME, October 2025), near 5-year lows

- Global mine supply: ~190,000 tonnes

- DRC share: 70%

- China refining share: 75%

- Top producers: Glencore, CMOC, ERG, Huayou Cobalt

So why was the U.S. tender canceled?

According to Bloomberg, industry sources said Washington struggled to attract bids that met both traceability and ethical sourcing rules. The U.S. government requires cobalt that is not sourced from Chinese-controlled supply chains and must meet Dodd-Frank conflict mineral standards.

That immediately eliminates most of the world’s cobalt.

The Democratic Republic of Congo (DRC) dominates supply, but China’s CMOC, Zijin, and Huayou control more than half of DRC output through joint ventures and offtake contracts. Alternative suppliers like Australia, Canada, Morocco, and Finland produce only modest tonnages in comparison — and most of it is already locked under long-term contracts to Chinese buyers.

The Pentagon’s procurement system simply ran into math: there isn’t enough non-Chinese cobalt in the world to meet U.S. stockpiling targets.

Strategic Risk

- U.S. has zero refining capacity for cobalt sulfate used in EV batteries

- The only U.S. cobalt miner, Jervois Global, placed its Idaho mine on care and maintenance in 2023 due to low prices

- No commercial-scale U.S. cobalt refining is currently operating

Why it matters: Defense supply chain vulnerability

This isn’t an EV story — it’s national security. Cobalt is used in superalloys critical to turbine blades in F-35 jets, Tomahawk cruise missiles, naval engines, and hypersonic propulsion components. The U.S. Department of Defense lists cobalt as a “single-point failure risk.”

The canceled tender signals that Washington is still unprepared for mineral conflict with China. Beijing has already used raw materials as leverage:

- In 2023, China restricted gallium and germanium exports

- In 2024, it imposed export licenses for graphite

- In 2025, China tightened control over rare earth magnets, slashing U.S. imports by 93.3% in May according to U.S. trade data

Cobalt could be next.

Market implication: bearish now, bullish long term

Cobalt prices collapsed from $40/lb in 2022 to ~$15/lb today due to oversupply from Indonesia and weaker-than-expected EV sales. But strategic demand is rising even as ESG requirements fragment the market into two supply chains: China-integrated cobalt and non-Chinese cobalt eligible for Western defense and EV markets.

Only the latter will command a premium — and there isn’t enough of it.

Can the U.S. fix this?

Not quickly. The U.S. has no coherent industrial policy for cobalt. The canceled tender proves stockpiling won’t work without upstream control. The U.S. strategy depends on three fragile pillars:

| Policy Pillar | Status |

|---|---|

| Domestic mining | stalled |

| Refining capacity | negligible |

| Allied sourcing | limited |

To regain ground, Washington would need to:

- Fast-track permitting for cobalt mining in Idaho and Minnesota

- Co-fund refining capacity in North America

- Underwrite offtake contracts to de-risk projects

- Secure DFCs loan guarantees for cobalt projects in Australia, Canada, and Morocco

- Negotiate cobalt supply corridors with the DRC and Zambia that bypass Chinese offtake

Why this story matters

- This is a choke point in U.S.–China competition

- Stockpiling is failing without supply control

- Cobalt market now bifurcating into China vs. West

- Traceable cobalt premiums are coming

Conclusion

The canceled cobalt tender is more than a procurement hiccup — it is a signal. The U.S. is not ready for a serious competition over critical minerals. China has already built the infrastructure, secured the resources, and locked down refining. Washington is still writing tenders.

This failure accelerates the weaponization of minerals. Cobalt is not optional. It is a strategic dependency. If the U.S. wants energy security, defense resilience, or competitive EV manufacturing, it must build cobalt supply chains outside China — fast.