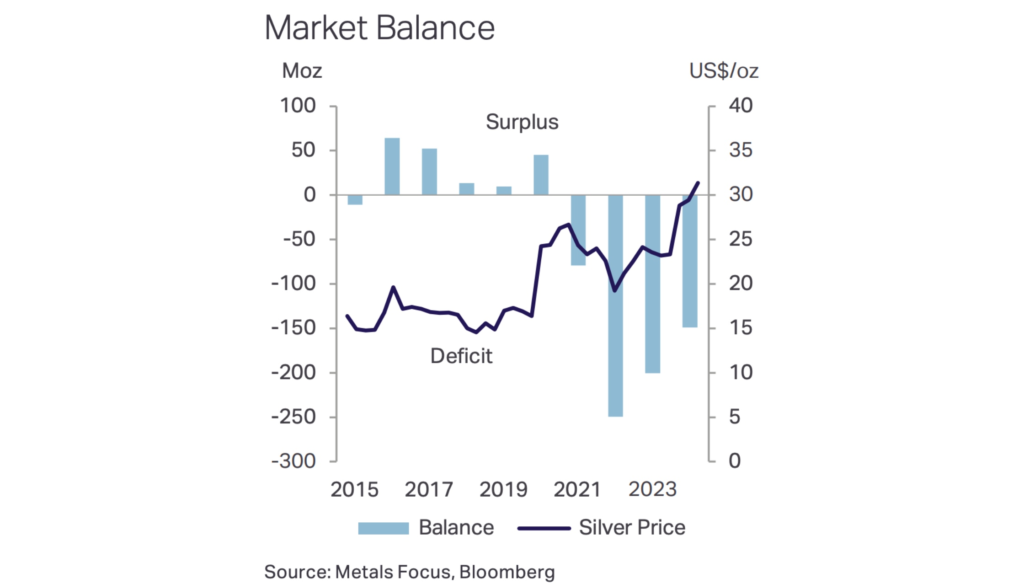

The global silver market remains in the grip of a persistent supply-demand imbalance, according to the newly released World Silver Survey 2025. For the fourth consecutive year, demand for silver has outstripped supply, with 2024 closing on a structural deficit of 148.9 million ounces (Moz)—and the gap is expected to remain stubbornly wide in 2025.

Demand: Industrial Boom Meets Investment Slump

Total silver demand slipped 3% in 2024 to 1.16 billion ounces, but that headline number masks a powerful undercurrent: industrial demand surged to a record 680.5 Moz, driven by the green economy’s relentless appetite for silver in solar panels, vehicle electrification, and grid infrastructure. Artificial intelligence and booming consumer electronics shipments added further fuel to the fire. China led the industrial gains with a 7% jump, while India rose 4%.

Yet, not all demand sectors shared in the upside. Physical investment—bars and coins—fell 22%, hitting a five-year low as profit-taking and market saturation swept through Western markets, particularly the US, where demand collapsed by nearly half. Jewelry and silverware demand also softened, with India’s consumers pulling back amid high prices, and Western buyers feeling the pinch from cost-of-living pressures.

Supply: Mining Flatlines, Recycling Climbs

On the supply side, mine production eked out a modest 0.9% gain to 819.7 Moz. The lion’s share came from lead/zinc mines, though output was flat year-on-year. Gold mines, by contrast, posted a 12% jump in silver byproduct, reflecting the impact of strong gold prices. Mexico retained its crown as the world’s top silver producer, with China and Peru following.

Recycling offered the only real supply-side dynamism, surging 6% to a 12-year high of 193.9 Moz. The main driver: industrial scrap, especially from spent ethylene oxide catalysts, and a wave of silverware and jewelry recycling as high prices and economic stress prompted selling in Western markets.

Deficit: Above-Ground Stocks Erode, Outlook Remains Tight

Despite robust recycling, the silver market remains in deficit. The World Silver Survey forecasts a 2025 shortfall of 117.6 Moz—still substantial, if down from 2024’s figure. Analysts warn that above-ground stocks, mainly in London, New York, and Shanghai, have been drawn down to bridge the gap, depleting inventories by nearly 800 Moz over the past four years—equivalent to an entire year’s mine supply.

The stakes are high. With mine output unlikely to rise meaningfully (and forecast to peak in 2026 before declining), the market’s persistent deficits will increasingly have to be met from dwindling secondary supplies and private holdings. As one analyst put it, “It’s the perfect storm: flat supply, growing demand, and shrinking stockpiles.”

Risks and Price Action: Tariffs, Geopolitics, and Volatility

The Survey flags US tariffs and global trade tensions as key risks for 2025. Extended or escalating tariffs could disrupt supply chains and drag on global GDP, potentially weighing on industrial, jewelry, and silverware demand—but could also stoke safe-haven investment if economic uncertainty deepens.

Silver prices reflected the market’s crosscurrents, surging 21% in 2024 and breaking above $34 per ounce in early 2025 before easing back on tariff news. With fundamentals and geopolitics aligned, many expect volatility to persist—but with the market’s structural deficit and robust industrial demand, the long-term bias remains upward.

Bottom Line

The World Silver Survey 2025 paints a picture of a market squeezed by relentless industrial demand and chronically tight supply. As above-ground inventories dwindle and mine production stagnates, the silver market’s next act may well be shaped by how quickly new supply can come online—or how high prices must go to balance the scales.