📌 Key takeaways

- The U.S. and Australia have lined up more than A$5 billion (US$3.5 billion) for critical minerals projects, spanning rare earths, nickel, graphite, tungsten and gallium, in a sign that allied supply chains are moving from rhetoric to capital deployment.

- The U.S., EU and Japan are now working on action plans, trade coordination and possible price support mechanisms to reduce dependence on China in critical minerals processing and supply.

- This is no longer just about mining more material. It is about who finances, refines, stockpiles and guarantees demand outside China.

- For investors, the signal is clear: projects in allied jurisdictions with downstream relevance and policy support now look more strategic than standalone resource stories.

⛏️ A new critical minerals bloc

The U.S. is starting to build a critical minerals bloc, with deals across key partners.

Washington and Canberra expanded joint support for Australian critical minerals projects to more than A$5 billion, or about US$3.5 billion. The package covers projects across rare earths, nickel, graphite, tungsten, magnesium, vanadium, scandium and gallium, with backing from Export Finance Australia and the U.S. Export-Import Bank.

But this is bigger than Australia. The U.S. is now moving in parallel with Japan, the European Union and other partners to build a supply chain system less exposed to China.

In February, 55 countries attended a U.S.-hosted ministerial on critical minerals, including Japan, South Korea, India, Germany, Australia and the Democratic Republic of Congo.

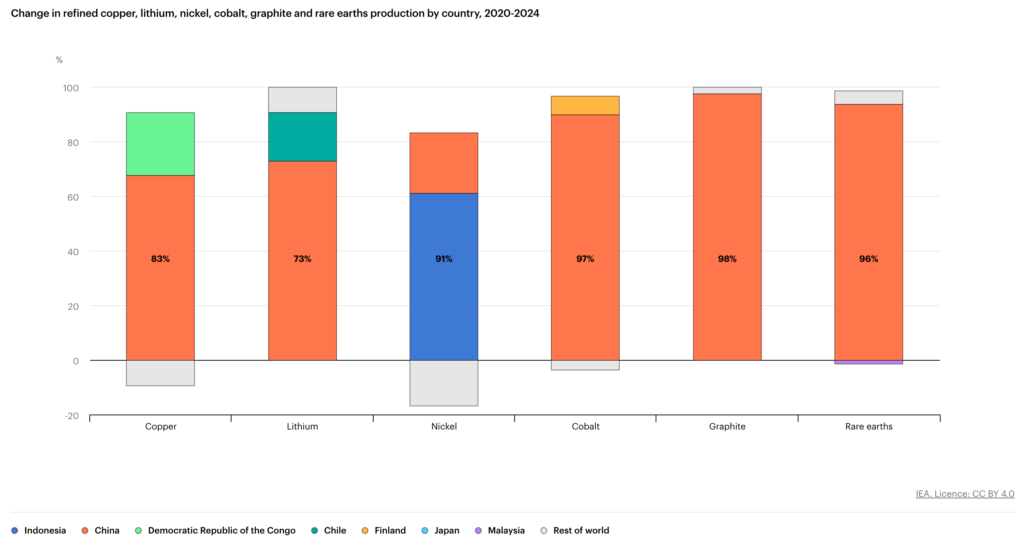

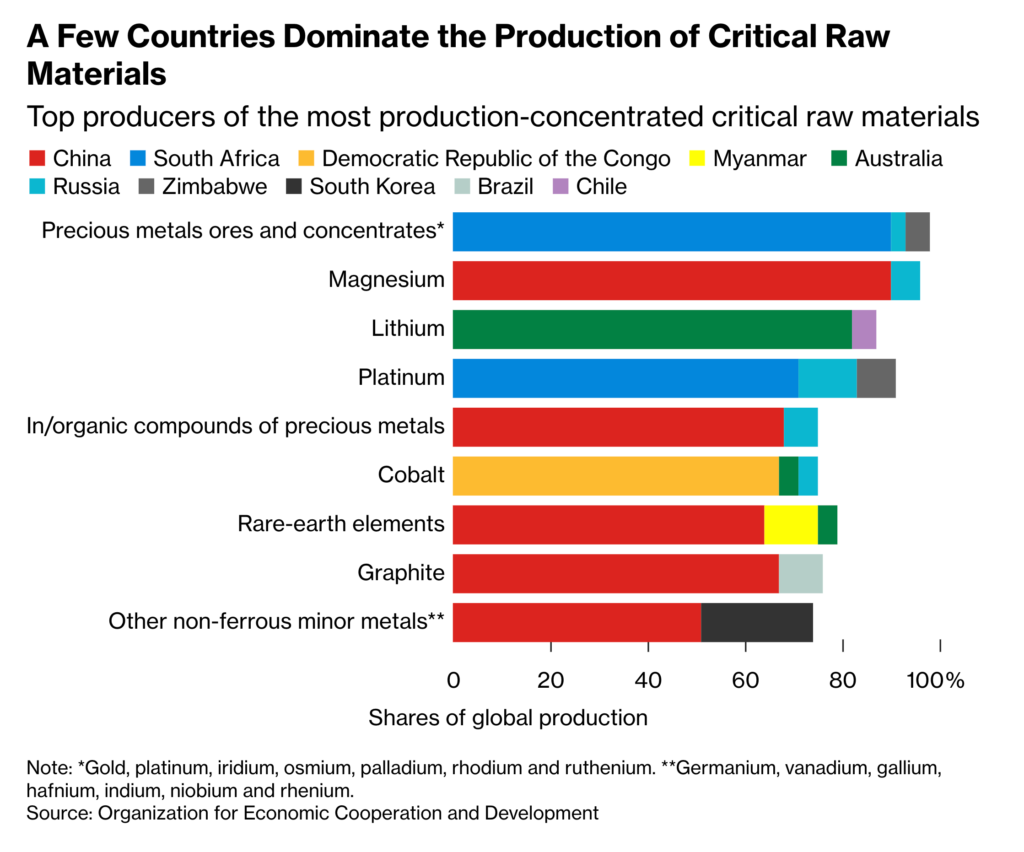

That matters because China still dominates the middle of the chain, with China is the dominant refiner for 19 of the 20 major critical minerals, holding an average market share of around 70%. The response from Washington is no longer just to approve more mines. It is to reshape the economics of non-Chinese supply.

The U.S. and EU are also close to a critical minerals deal aimed at reducing Chinese control, with the draft plan covering standards, investment coordination, joint projects and possible incentives for non-Chinese suppliers. Japan is moving on a similar track. USTR said in March that the U.S. and Japan had enacted an action plan covering strategic trade policy, stockpiling coordination, disruption response and cooperation against economic coercion.

Australia is the clearest test case because it combines geology, political alignment and now capital support. Reuters said the latest U.S.-Australia package includes backing for projects such as Tronox’s rare earths refinery, Ardea Resources’ Kalgoorlie Nickel Project, Alcoa’s gallium recovery plans and Arafura’s Nolans rare earths development. That is notable because the backing is not just going into mines. It is also flowing to processing capacity, where China still holds the strongest leverage.

🚨 Why it matters

Critical minerals are becoming less like a normal commodity market and more like a strategic market for national security.

If the U.S., EU, Japan and Australia move ahead with public finance, stockpiles, floor prices and coordinated offtake support, then allied projects may no longer be valued only on spot economics. They may be valued on strategic fit.

That changes the screen for investors. Grade still matters. Scale still matters. But so do jurisdiction, refining optionality, financing access and geopolitical alignment.

The likely winners are not every company with a critical minerals resource. They are the projects that solve a real bottleneck inside an allied supply chain.