📌 Key Takeaways

- The Strait of Hormuz handled about 20 million barrels per day in 2024, equal to roughly 20% of global petroleum liquids consumption, and about 20% of global LNG trade, making it a global chokepoint.

- The U.S. remains dangerously exposed as it is 100% net import reliant for 12 critical minerals and more than 50% reliant for another 28 in 2024.

- The immediate winners from Hormuz disruption are obvious: U.S. fuel exports hit a record 3.11 million bpd in March, while U.S. LNG exports hit a record 11.7 million metric tons.

- The war is not just higher oil, but a shipping shock is making reshoring mining, processing, stockpiling and recycling look less like industrial policy and more like basic economic security.

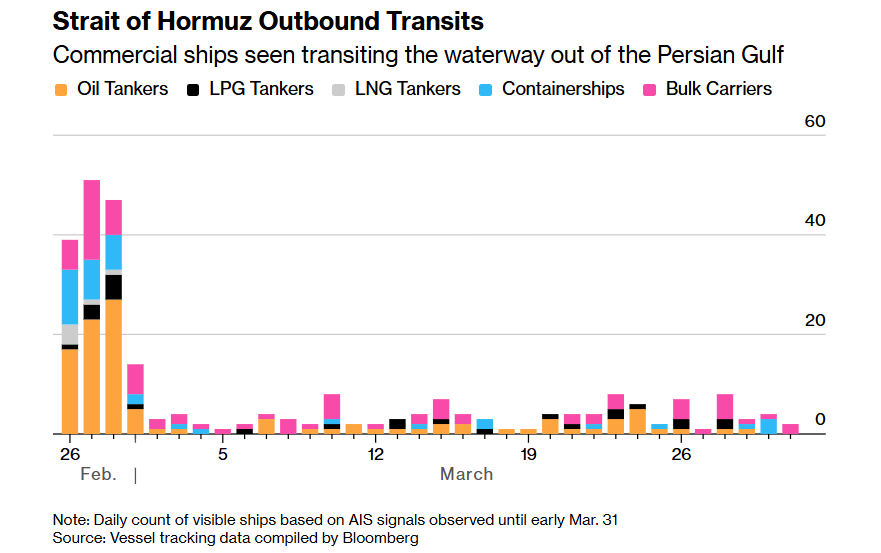

In 2024, oil flows through the passage averaged 20 million barrels per day, equal to about one-fifth of global petroleum liquids consumption. In LNG, roughly one-fifth of global trade also moved through Hormuz, overwhelmingly from Qatar and the UAE.

Now, the IEA says the Middle East war has created the largest supply disruption in the history of the global oil market, with flows through Hormuz plunging from around 20 mb/d to a trickle and export volumes of crude and refined products falling to less than 10% of pre-conflict levels.

That matters for U.S. critical minerals and mining for a simple reason: most people still think reshoring is about China. It is. But Hormuz shows it is also about fuel, feedstocks, freight, insurance, sulphuric acis and whether the West can still run an industrial system when one waterway shuts.

⛽ Why does Hormuz matter for critical minerals, not just oil?

Mining is an energy business first, and a geology business second.

Diesel runs haul trucks, excavators, drills, generators and logistics chains. LNG and gas matter for power, fertilizer and industrial heat. Aluminium, sulfur, ammonia and refined fuels all sit somewhere in the middle of the minerals value chain.

When Hormuz tightens, it does not just lift Brent. It pushes up the cost of moving rock, processing ore and building everything from smelters to data centers.

Last week that Singapore diesel swap prices had nearly doubled to more than $180 per barrel from $92.5 before the conflict. Fortescue said every 10-cent rise in diesel prices adds about $70 million to its costs and roughly $500 million to the combined costs of the top four miners.

That is the first-order effect.

The second-order effect is more important. The IEA says only Saudi Arabia and the UAE have operational crude pipelines that can partly bypass Hormuz, with just 3.5 mb/d to 5.5 mb/d of spare capacity. For LNG, there are effectively no alternative routes for the volumes that normally leave Qatar and the UAE through the Strait.

That means industrial users do not just face higher prices, but also face genuine physical insecurity:

- Fuel for mines and heavy industry gets more expensive fast.

- LNG-dependent manufacturers lose flexibility because rerouting options are limited.

- Aluminium and other upstream materials become harder to source on time.

- Investors start paying for proximity, not just grade or scale. This is an inference from the trade and cost data.

⛏️ How exposed is the United States on critical minerals?

Very exposed.

USGS says the United States was 100% net import reliant for 12 of the 50 minerals on the 2022 critical minerals list, and more than 50% net import reliant for another 28.

The list includes some obvious weak points. The U.S. was 100% import reliant for gallium metal and natural graphite, with China among the leading import sources for both.

Rare earths look only slightly better. The USGS rare earths chapter says U.S. net import reliance for rare-earth compounds and metals was 80% in 2024, while China accounted for 70% of U.S. import sources for rare-earth compounds and metals in 2020-23. And, in 2025, in retaliation for Trump’s tarrffs, China introduced export restrictions on rare earths — bringing the USA back to the negotiating table.

What was already a strategic vulnerability is now compounding.

If the U.S. is exposed to China in refining, exposed to Hormuz in global energy markets, and exposed to global shipping in the middle, then the old model of “mine somewhere, process somewhere else, ship through whatever route is open” starts to look fragile.

🇺🇸 Why does this strengthen the case for U.S. reshoring?

When energy is cheap and freight is smooth, offshore supply chains often win on cost. When a war can take a fifth of global LNG trade and a fifth of petroleum liquids demand-equivalent flows off the table, the calculation shifts. Security of supply starts to have a cash value — which was already happening as te US was still just making preparations for the war.

For example, in January, Washington has launched Project Vault, a $12 billion U.S. strategic critical minerals reserve backed by $10 billion in EXIM financing and $2 billion from the private sector. The administration has also pushed a broader critical minerals club with allied countries.

The direction is clear. More stockpiling. More offtake support. More allied sourcing. More domestic processing. More tolerance for paying up for resilience.

The clearest new warning is aluminium. The IEA notes that the Gulf region produces around 8% of global aluminium supply, and about 5 million tonnes a year move through the Strait from smelters in Bahrain, Qatar, Saudi Arabia and the UAE. Reuters reported that attacks on major Middle East smelters have punched a hole in the U.S. aluminium supply chain because the U.S. does not produce nearly enough of the metal domestically.

That same logic applies across battery materials, magnets, specialty metals and semis inputs.

That makes sense. The crisis in the Strait of Hormuz argues for:

- Not just mining ore in the U.S.

- Building refining and separation capacity near end markets

- Locking in stockpiles and long-term offtake

- Recycling materials already inside the U.S. economy

- Treating energy security and mineral security as the same issue

💰 Which U.S. sectors benefit?

Let’s start with energy.

Reuters reported that U.S. clean fuel exports rose to a record 3.11 million bpd in March as Asia and Europe scrambled to replace disrupted Middle East supply. Exports to Europe rose 27%, shipments to Asia more than doubled, and flows to Africa jumped 169%.

U.S. LNG did the same. March LNG exports hit a record 11.7 million metric tons, while the U.S. cemented its position as the world’s largest LNG exporter. EIA says U.S. LNG exports rose from 0.5 Bcf/d in 2016 to 15.0 Bcf/d in 2025, and forecasts they could exceed 18.1 Bcf/d in 2027.

Look at the projects now being pushed as ways to shorten or harden U.S. supply chains. Before the war, the groundwork was already there: Syrah’s Vidalia plant in Louisiana began commercial spherical graphite production with initial capacity of 11,300 tonnes per year and a planned expansion to 45,000 tonnes; MP Materials stopped sending rare earth concentrate to China for processing; Perpetua’s Stibnite project won its final federal permit; and the White House moved to fast-track 10 mining projects across the country.

And, since the war began, the U.S. push has moved from broad rhetoric to a mix of emergency procurement, project acceleration and new supply-chain tie-ups:

- REalloys + U.S. Critical Materials (April 1, 2026): the two companies signed an MoU to build a fully domestic rare earth supply chain around the Sheep Creek deposit in Montana, with REalloys securing up to 10% offtake and the partnership focused on heavy rare earths including dysprosium and terbium. Reuters framed it explicitly as part of the effort to cut China out of a strategically sensitive chain.

- Pentagon solicitation for 13 critical minerals (reported March 4, 2026): one day before the Iran strike, the U.S. military asked mining companies to propose ways to boost domestic supply of 13 critical minerals used in semiconductors, weapons and other products. That matters because it shows Washington was already shifting into a wartime footing on materials before the regional shock fully hit energy and shipping.

- USA Rare Earth moves to consolidate Round Top (March 5, 2026): USA Rare Earth said it would buy the remaining stake in the Round Top project in Texas, which Reuters described as the largest known U.S. source of heavy rare earths, gallium and beryllium. The company said it wants commercial production by late 2028, ahead of the previous 2030 timeline, helped by a proposed $1.6 billion debt-and-equity package for the mine and magnet facility.

- Glomar Minerals + Cobalt Blue U.S. refinery plan (March 29, 2026): the partners said they want to build a U.S.-based refinery for critical minerals recovered from Pacific polymetallic nodules, with an initial processing target of 200,000 metric tons a year and a project cost of under $500 million. It is not a conventional mine reshoring story, but it is still part of the broader U.S. effort to localize processing capacity.

- Rhyolite Ridge legal win (March 30, 2026): a federal judge upheld the government’s approval of ioneer’s Nevada lithium-boron project, removing one of the biggest legal overhangs on a mine seen as an important future domestic lithium source. Reuters noted the project had previously won a $996 million U.S. government loan commitment, even though ioneer is still seeking a new partner after Sibanye withdrew.

The market signal is straightforward. In a world where both Beijing and Hormuz can disrupt supply, U.S. projects no longer need to beat the cheapest global source on a static cost curve. They need to beat the cost of strategic failure.

Import-dependent manufacturers that still assume global markets will always clear.

So the U.S. now faces two overlapping realities. China can squeeze the refining side. Hormuz can squeeze the energy and shipping side. The companies caught between them are the ones still betting on just-in-time globalization.

📣 What is the bigger strategic shift?

The Strait of Hormuz closure does not create the U.S. reshoring story. It accelerates it.

For years, the debate was framed around China’s grip on critical minerals processing. That was already enough to justify more domestic mining and refining. But Hormuz widens the case. It shows that the West’s problem is not one dependency. It is stacked dependencies: foreign fuel, foreign shipping lanes, foreign refining, foreign midstream chemicals, foreign inventories.

That is why the real U.S. response is likely to be broader than mine permitting alone. Expect more focus on:

- domestic fuel and power resilience for industrial sites,

- local refining and separation,

- recycling as a strategic source of supply,

- stockpiles for both minerals and fuels,

- and allied supply chains that route around both China and Hormuz.

The investment takeaway is simple. The Strait of Hormuz closure makes “reshoring critical minerals” sound less like a slogan and more like a balance-sheet necessity. In that world, U.S. energy exporters, domestic processors, strategic metal projects and companies that can shorten supply chains should command a premium. Everyone else is now paying to learn what chokepoint risk really costs.