📌 Key Takeaways:

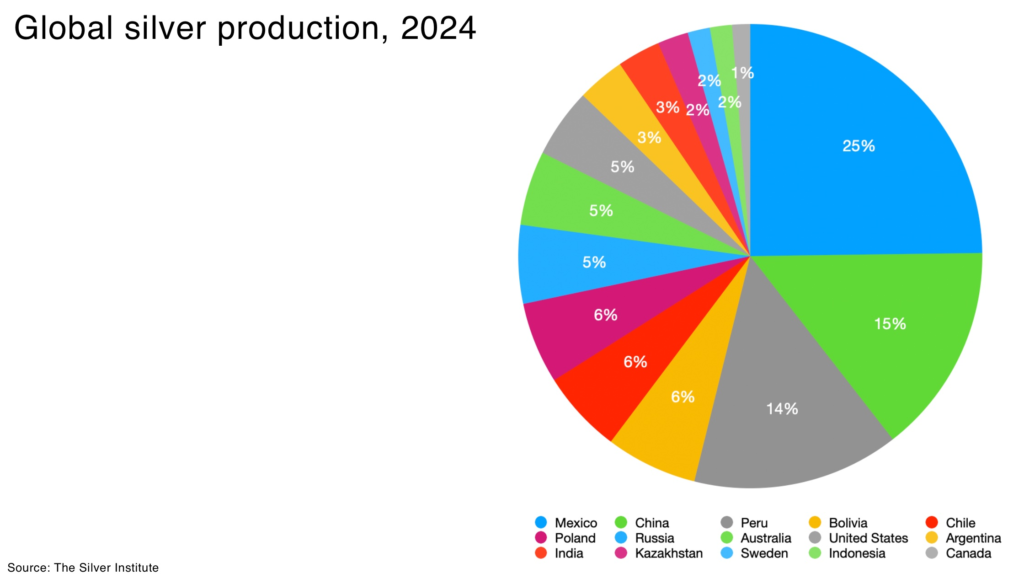

- Top Producer Under Pressure: Mexico is the world’s largest silver producer, accounting for ~24% of global mine output.

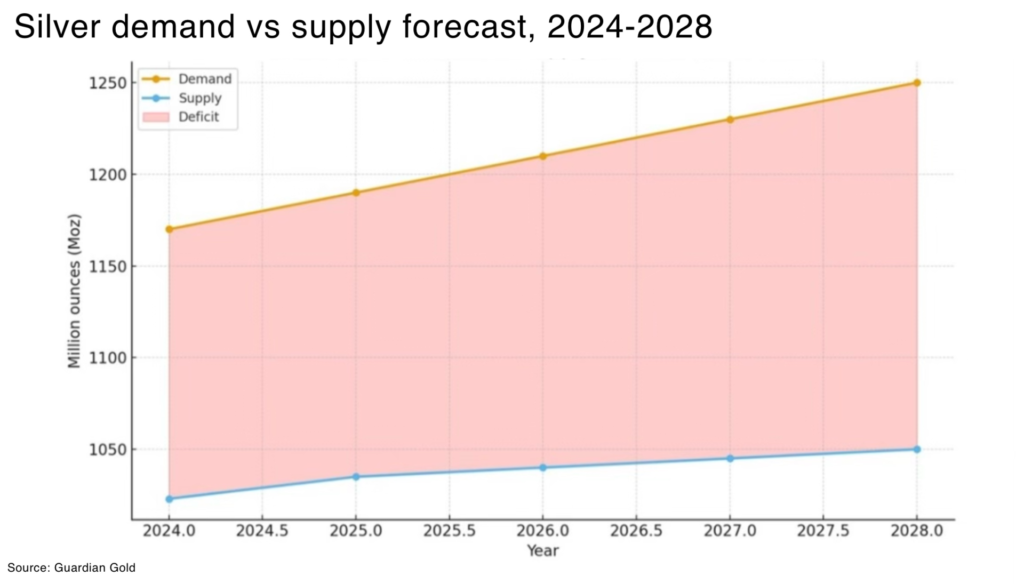

- Surging Demand, Supply Squeeze: The silver market has been in deficit for seven consecutive years, amid a clean-tech boom has turbocharged silver consumption for solar panels, electric vehicles, and electronics.

- Investment Rebounds on Policy Reset: In mid-2024, within weeks of Mexico’s election, two major deals worth over $2.5 billion were announced into Mexican silver mining.

- Risks: Policy and Sustainability: The new government under President Claudia Sheinbaum is signaling a more pragmatic, pro-investment stance than her predecessor. Legacy anti-mining measures are being reconsidered.

Can Mexico meet surging silver demand?

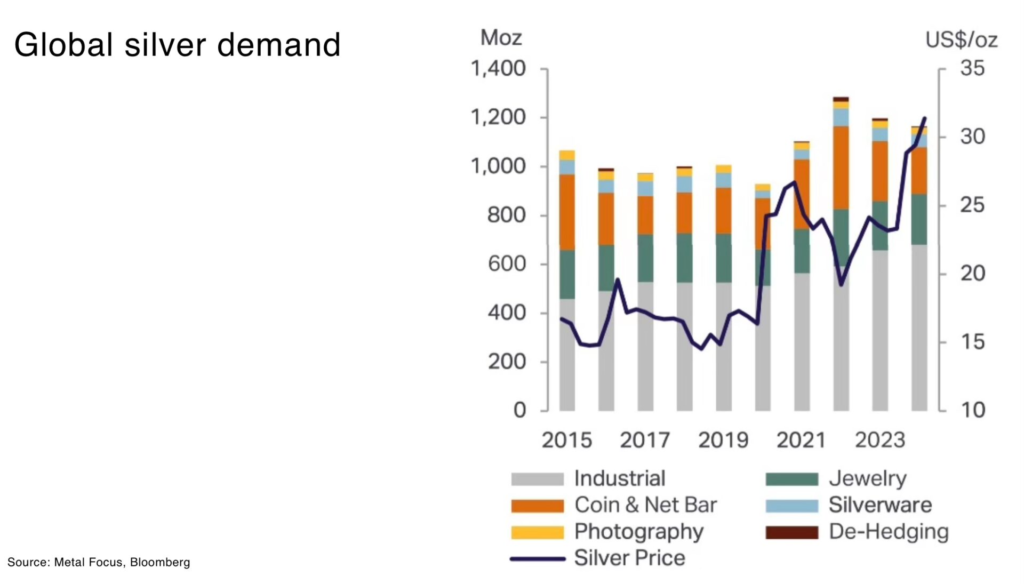

Global silver consumption is running at all-time highs, driven by industrial and precious metal demand, just as supply struggles with a structural supply deficit for the past seven years.

In 2023, the silver supply shortfall was an estimated 184 million ounces, following a record 253 Moz deficit in 2022. The Silver Institute projects the deficit will continue in 2026.

This sustained squeeze has provided a potent tailwind for prices with silver rallying to more than $70 per ounce in December 2025.

Mexico, as the source of nearly a quarter of the world’s silver, is central to securing new silver supply.

With silver prices at record highs and a deepening global supply deficit, investors are prioritizing jurisdictions with shovel-ready projects and low capital intensity. Mexico stands out, not just for its geology but for its infrastructure, skilled workforce, and proximity to U.S. industrial demand. Dozens of silver deposits, which are already permitted or in late-stage development, offer quick timelines to production and sub-$200M capex profiles.

After years of caution over the Mexico story, the country now presents a rare combination of scale, speed, and strategic relevance that’s difficult to replicate elsewhere.

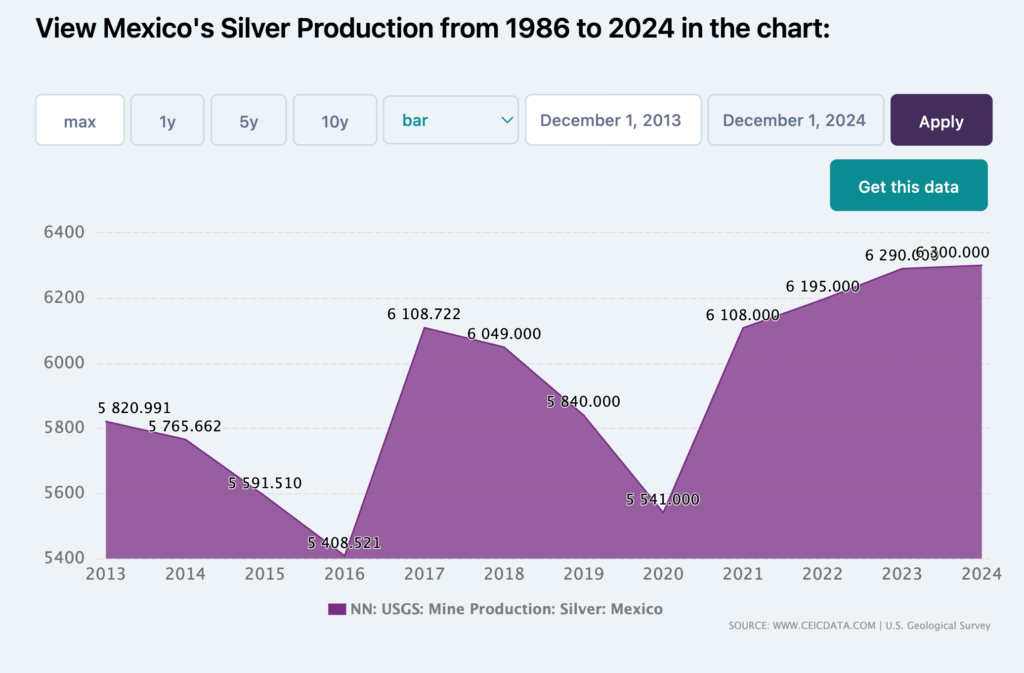

The challenge for investment into Mexico before June 2024, particularly in the mining industry, has been regulatory and political risk. This risk meant Mexican mines produced roughly 202.2 Moz of silver, yet that output fell ~5% year-on-year, with mining investments decreasing 5.8% in 2023 year-on-year.

For much of the past six years, Mexico’s mining sector was clouded by policy uncertainty. Former President Andrés Manuel López Obrador (AMLO) froze the issuance of new mining concessions since 2018, tightened environmental regulations, and even pushed to nationalize lithium resources. A sweeping mining reform passed in 2023 slashed concession terms (to 30 years from 50) and threatened tougher rules on water use and permits. Talk of banning open-pit mining outright sent further chills through the industry, particularly given that many of Mexico’s largest gold-silver mines (and copper operations) are open pits.

A four-month workers’ strike at Newmont’s Peñasquito mine, one of the country’s biggest silver sources, also impacted production. The Peñasquito stoppage in mid-2023 alone temporarily erased tens of millions of ounces from Mexico’s production tally.

However, the uncertainty now seems to be over, and investment is responding.

So, what’s changed?

Why are miners betting on Mexico again?

In June, 2024, the election of President Claudia Sheinbaum (AMLO’s successor from the same party) initially signaled continuity, but in practice has opened the door to a more pragmatic, investment-friendly approach.

Sheinbaum’s new administration has moved to restore industry confidence. Notably, Sheinbaum also omitted AMLO’s proposed open-pit mining ban from her early policy agenda, despite campaign rhetoric.

The new administration’s economy minister, former diplomat Marcelo Ebrard, is viewed as a moderate focused on attracting foreign investment. At a recent press conference, Minister of Economy Marcelo Ebrard announced that the approval processes for mining projects would be further accelerated in 2026.

A backlog in the issuance of mining permits accumulated over the past four years in Mexico has reportedly been reduced by about 50% as of 2025. Fernando Aboitiz, Head of the Coordination Unit for Extractive Industries at the Ministry of Economy, explained at the XXXVI International Mining Convention 2025 that 176 previously blocked permits in the mining sector are awaiting a decision, which could unlock investments of around $7 billion.

Mexico’s environment ministry is reportedly currently reviewing official standards and regulations on mining activities, without leading to “overregulation.” The federal government has also reactivated environmental and water permit issuance.

According to the Fraser Institute annual survey of mining companies, Mexico increased its Investment Attractiveness Index score by almost 18 points and climbed to the 49th spot (of 82) after ranking 74th (of 86) last year.

Crucially, this political shift has coincided with a renewed investor appetite for Mexican silver assets.

Within weeks of the June 2024 vote, over $2.5 billion in M&A deals were announced, targeting high-grade silver operations in Mexico:

- Coeur Mining’s $1.7 billion acquisition of SilverCrest Metals (owner of the Las Chispas mine in Sonora)

- and First Majestic Silver’s $970 million purchase of Gatos Silver (operator of a Chihuahua silver mine)

These deals, among the largest in the silver space in years, effectively circumvented AMLO’s concession moratorium by consolidating existing projects, and underscored a vote of confidence in Mexico’s mining sector.

Beyond M&A, fresh capital is eyeing new developments. In the second half of 2024, multiple Canada-based miners announced plans to launch new silver projects in Mexico within 6–12 months. For example, Silver Storm Mining has partnered with subsidiaries of technology giant Samsung for offtake prepayment financing to restart the past-producing La Parrilla silver mine, in Durango, Mexico; Endeavour Silver‘s US$332mn Terronera gold-silver project in Jalisco state was 89.4% complete at the end of 2024, with US$302mn having been spent, according to Camimex; the silver projects planned for start-up this year are Terronera, Media Luna and La Preciosa, while Cordero, El Tigre and Los Ricos Sur are expected to enter production next year.

Mexico’s central bank noted that by mid-2024, the mining sector was growing again – non-oil mining GDP rose over 9% year-on-year in July, helped by rising output of silver, gold, copper, and zinc.

On the geopolitical front, Mexico’s role as a stable source of critical minerals is increasingly in the spotlight. The United States, which imports more silver from Mexico than from any other country (nearly three times the volume from Canada), views Mexican silver supply as vital for high-tech manufacturing, renewable energy, and defense, especially as the US-China trade war continues.

“Mexico’s silver endowment is unmatched, and with prices where they are, projects that were marginal two years ago are now economically compelling. The key is clarity. As the new administration continues to stabilize permitting, capital will follow.

Apollo Silver is strategically positioned as a silver developer with exposure to both U.S. and Mexican supply chains. While advancing its flagship Calico Project in California, one of the United States’ largest undeveloped primary silver assets, the Company also sees potential near-term upside from its Cinco de Mayo Project in Chihuahua, Mexico. Cinco de Mayo hosts a large, high-grade carbonate replacement deposit (“CRD”) system, benefits from established regional infrastructure, and is located in a historic mining district with a long production track record. The Company looks forward to advancing the project as it works toward securing social license through continued community engagement. This effort is supported by a team with deep operational experience in Mexico”

– Ross McElroy, CEO, Apollo Silver TSX.V:APGO / OTCQB:APGOF

Of course, investing in Mexico is not without challenges. Some elements of the 2023 mining reform persist – shorter concession durations, higher taxes and royalties, and stricter environmental oversight will shape project economics. The spectre of an open-pit mining ban isn’t completely dead, as legislation to prohibit new open-pit mines continues to percolate in Congress.

Security is another concern. Organized crime groups do operate in some mining regions, primarily extorting transport routes, but seasoned operators note the risk is “manageable” with proper precautions. Several key mining states (like Sonora, Zacatecas, Chihuahua) have a strong security apparatus and a culture of cooperation with the industry to deter cartel influence.

Strong Foundations, Despite Volatility

Despite any policy swings, Mexico’s mining sector primarily rests on deep institutional advantages that new investment can leverage:

- Established mining culture and skilled workforce with decades of experience across silver, gold, and base metals.

- Legal system rooted in civil law principles, familiar to international investors and offering a baseline of contractual stability.

- Decentralized permitting: key mining states like Sonora, Chihuahua, and Zacatecas wield significant autonomy—unlike centralized jurisdictions such as Ecuador—allowing smoother project approvals at the state level.

- Trade protections under USMCA: When the AMLO administration moved to nationalize lithium, the U.S. triggered dispute resolution mechanisms, adding a layer of enforceable legal security for foreign investors.

The result: while regulatory risk remains, Mexico offers one of the most developed, resilient mining ecosystems in the Americas, positioned to scale quickly in a high-price environment.

Silver Demand

Mexico in a pivotal position, between expanding demand, tightening supply and a critical geopolitical location.

IEA Solar PV Global Supply Chains states that in its NZE scenario, 2030 PV silver demand could exceed 30% of total global silver production, up from 10% in 2020. This is a scenario that would strain miners without major new investment.

Outlook

With a structural bull market in silver underway, underpinned by the twin engines of scarcity and indispensable industrial demand, as well as liquidity through financial pressures, Mexico’s silver industry is positioned for significant opportunity.

Capital is flowing back, new mines are in the pipeline, and Mexico’s status as the silver juggernaut of the Western Hemisphere is looking increasingly secure.

The extent to which Mexico can capitalize on this moment will depend on policy consistency and on-the-ground execution — which would allow Mexico to not only maintain its silver supremacy but potentially expand output to meet the world’s growing demand.

Mexico’s macro environment for silver is markedly brighter entering 2025, with high prices, improving politics, and robust demand aligning to potentially spark a new silver renaissance in the country.