📌 Key takeaways

- A new report from Fitch Solutions BMI forecasts a supply-driven deficit in refined tin markets, raising its 2026 tin price forecast to US$ 35,000/t from a prior US$ 32,000/t.

- Supply remains tightly constrained: major producers in Indonesia face persistent permit delays and export-control risks, while upstream ore flows from Wa State (Myanmar) remain unsettled.

- Demand from semiconductors, solar, EV electronics and data infrastructure continues to firm. That suggests tighter balances ahead if supply disruptions persist.

Fitch Solutions BMI’s latest market dispatch warns the global tin market is moving into deficit. The firm lifted its 2026 price forecast to US$ 35,000 per tonne — up nearly 10 % — citing a “thin pipeline” of concentrates and shrinking refined output as key risk factors.

That projection carries extra weight given tin’s supply structure: just a handful of smelters now dominate global output, making the metal unusually sensitive to upstream disruptions.

Why supply remains locked

Indonesia & Myanmar still key supply pressure points

Indonesia — historically the world’s largest exporter of refined tin — continues to struggle with mining-permit delays and export constraints.

Meanwhile, ore supply from Wa State, long a major tin concentrate source for China’s smelters, remains uncertain. Despite occasional restart announcements at major mines, actual volumes shipped remain erratic or delayed.

Bottlenecks in smelting and refining

Smelting capacity cannot simply be switched on overnight. With limited concentrate feed, many refining operations in China are already reporting constrained throughput — a choke point that could force refined-tin output well below prior projections.

That structural supply tightness stands in contrast to typical base-metal cycles where demand weakness or market saturation cushions price swings.

Demand drivers remain steady

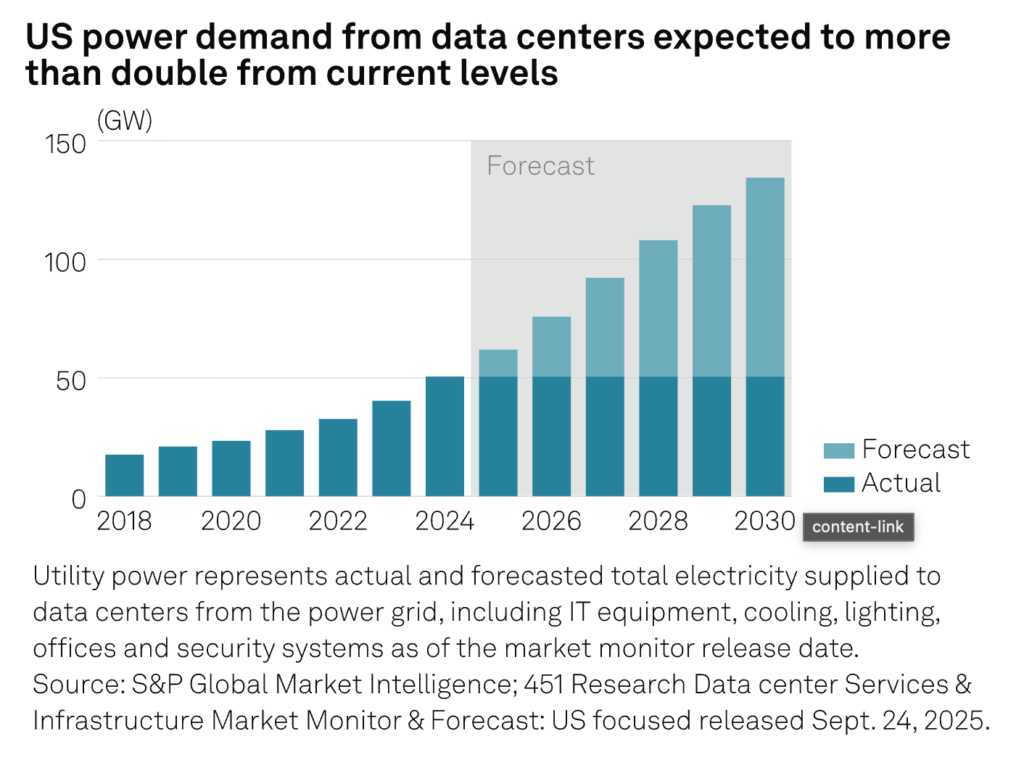

Tin’s traditional uses — electronics solder, wiring, packaging — remain stable. But growth is increasingly coming from high-tech and clean-energy sectors. Expansion of semiconductors, EV electronics, solar panels and data-centre hardware is pushing demand for refined tin upward. For example, serverboards connect the essential electrical components of a server and are 73% tin.

As global electrification and digitization intensify, tin’s role as a critical industrial metal is gaining strategic importance.