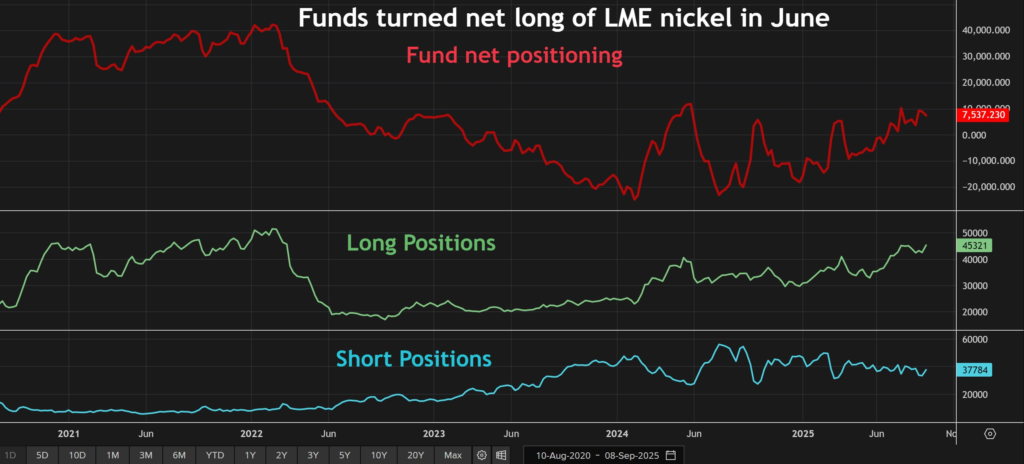

Hedge funds and other speculative traders have amassed long positions equivalent to 272,000 tons on the nickel price, the most optimistic stance since the March 2022 spike.

Nickel is sitting near a five-year low — around $15,000 per ton — after one of the sharpest collapses in base metals markets. Prices have halved from 2022’s chaos as a wave of Indonesian supply flooded the world. Yet against that backdrop of surplus and pessimism, investment funds have quietly flipped bullish.

The thesis of the investors is simple: nickel has hit rock bottom, and the downside is gone.

A Price on the Cost Floor

Nickel’s fall has been dramatic. The metal plunged roughly 40% over the past two years as new processing capacity in Indonesia overwhelmed demand. But prices have been stuck in a tight $14,800–$16,000 trading band this year despite worsening inventory data. Traders interpret that as a sign that the market has reached its floor.

That view aligns with producer economics. At current prices, around 40% of global production is loss-making, according to Macquarie. High-cost miners in Australia, Africa and Europe have already shuttered operations. An estimated 500,000 tons of non-Indonesian supply has come out of the market in recent years. Nickel outside Indonesia and China is now at its lowest level since 1990.

When a commodity reaches the point where large chunks of supply cannot operate, the logic is that the price is unsustainably low. That’s what funds are buying.

The Indonesia Problem

Nickel’s slump has a single source: Indonesia, now responsible for more than 60% of global output. It has built dozens of smelters and HPAL plants — with Chinese backing — and poured nickel into the market faster than demand could absorb it. In the first half of 2025, Indonesian production jumped 21% to 1.3 million tons.

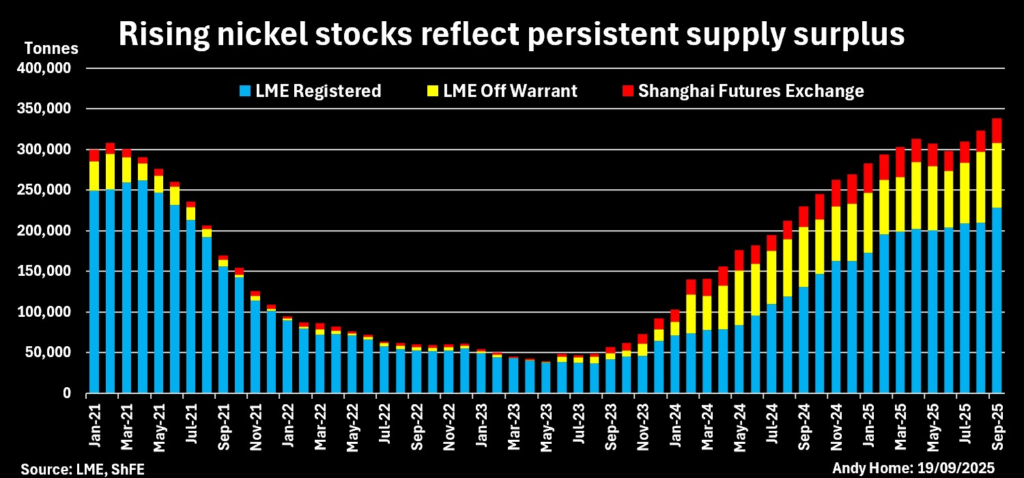

Exchange warehouses are overflowing. LME nickel inventories have surged to about 308,000 tons, the highest since 2020. Chinese-origin nickel now accounts for 65% of LME stocks (up from 0% two years ago) as Indonesian material feeds Chinese refineries before landing at the LME.

For Western producers, the result has been carnage: shutdowns at Australia’s Nickel West, closures across New Caledonia and southern Africa, and suspended refining capacity in Europe. If the glut continues at this pace, supply destruction will accelerate.

Should We Expect Production Discipline?

Funds see mounting evidence that Indonesia’s political calculus is shifting.

The government has warned that mining is running “too high above industry demand” and pushing prices to damaging levels. Regulators have begun seizing illegal mining sites and shortening licenses to one year, tightening control of output.

Most importantly, policymakers are considering a major quota cut: reducing planned nickel ore mining from 240 million tons to 150 million tons annually — almost 40% lower than previously intended. If enacted, that would finally cap the runaway expansion.

There are already hints of strain. Declining ore grades and weather disruptions have led to importing ore from the Philippines to keep Indonesian plants running — a telling reversal for the world’s dominant supplier.

If Indonesia slows down, even modestly, the surplus shrinks fast. That’s what speculative money is positioning for.

Demand: Less EV Hype, More Stainless Reality

Just two years ago, investors saw nickel as the core metal of the EV revolution. That story has cooled. Chinese automakers are boosting LFP battery use — chemistry that contains no nickel — because it is roughly 50% cheaper than nickel-rich cathodes.

Battery demand is still growing, but not explosively. The real backbone of nickel usage remains stainless steel, which accounts for ~65% of consumption【Macquarie†6†L1622-L1625】. Producers in China have seized the price slump as an opportunity to make more steel — a steady source of demand that sets a soft floor for nickel.

Meanwhile, China’s state stockpiling has absorbed excess metal. Government entities have reportedly purchased 100,000 tons of refined nickel since late 2024【Bloomberg†27†L53-L87】. Imports are growing faster than real usage — a sign Beijing is building buffer inventories rather than relying on market flows.

Stockpiling is not structural demand — but it buys time until fundamentals tighten.

Why Funds Are Buying

Funds are betting that:

- Cost support has created a firm floor around $15,000

- Supply attrition will continue outside Indonesia

- Indonesia may choose price over volume

- Stainless steel demand is rising into the weakness

- Any positive catalyst triggers a sharp rebound

With the consensus still bearish, markets are poorly positioned for upside. If Indonesia announces credible curbs, or if physical tightness starts to show through inventories, the snapback could be violent. Nickel’s history — and thin liquidity — favors sudden repricing.

No one expects a return to 2022 chaos. But recovering to a price that sustains more than 60% of global production? That’s a reasonable bullish case.

A Critical Metal Stuck in the Wrong Place

Nickel today illustrates a paradox of the energy transition: strategic dependence has grown even as prices collapse. Western governments want domestic or allied supply, but the economics don’t work when one country — Indonesia — controls the market and sets the price.

Funds are willing to wait for the turn. The question is whether countries that care about industrial resilience will do the same.

For now, the market message is clear:

Nickel is cheap — maybe too cheap. And the smart money is already positioned for what comes next.