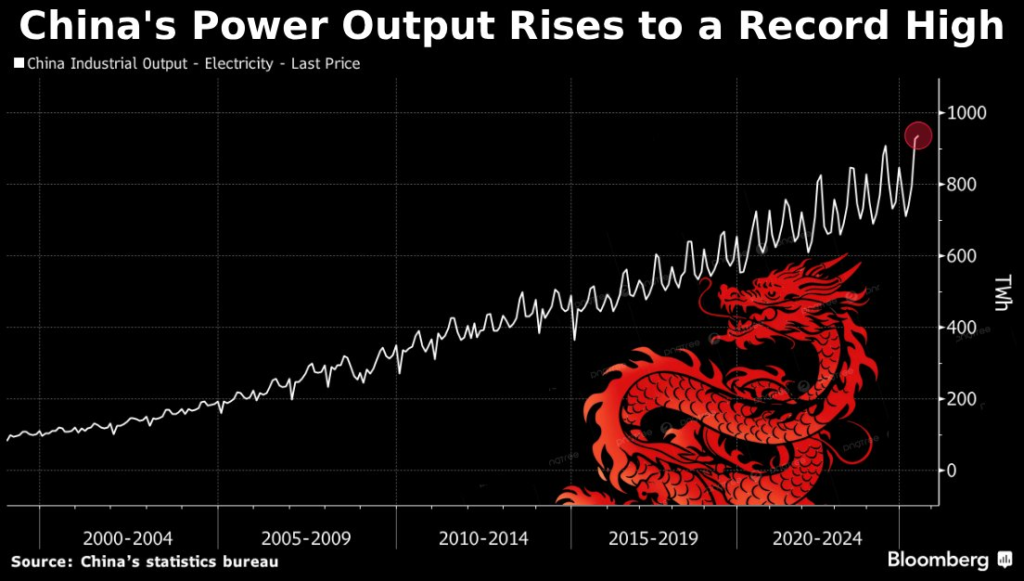

China’s power output hit 936TWh of electricity in August 2025 — with 627.4 TWh from thermal plants, meaning the most electricity it’s ever produced using coal — according to the country’s National Bureau of Statistics.

China’s electricity production for just one month is approx Japan’s entire annual output. The mix includes:

- 67%: fossil fuels

- 16%: hydro

- 13%: wind and solar

- 5%: nuclear

With extreme heat and weak hydro, China leaned on thermal (mostly coal) generation to meet the spike. Fossil-fuelled output hit 602 TWh in July, the highest since August 2024, as hydropower fell ~9.8% y/y on drought. Total generation rose 3.1% y/y to 926.7 TWh.

Why is coal demand so resilient in China?

National policy against the use of coal has tightened even as demand rose. August coal mine output fell ~3% y/y to ~390.5 Mt after safety inspections and curbs on over-mining — the second straight month of restraint. July output had already slipped to a 12-month low before rebounding slightly in August.

Yet capacity keeps expanding: China commissioned ~21 GW of new coal-fired power in H1’25, the highest first-half total in years, underscoring a “build-but-not-burn” strategy that prioritizes reliability during peak demand and hydrological stress.

Near-term coal burn tracks weather and hydro volatility; medium-term coal generation stays capped by administrative controls and air-quality goals, but capacity additions and record summer peaks keep a floor under domestic demand for high-availability thermal units and grid services.

Gas, oil, and the rest of the stack

Thermal reliance during heat waves lifts marginal demand for LNG and pipeline gas, especially in coastal provinces where gas peakers backstop renewables and faltering hydro. Reuters flagged fossil output at an 11-month high precisely as hydro weakened — a pattern that typically supports summer LNG spot draws if prices cooperate.

On oil, China continued building crude stocks in August — roughly >1 million b/d surplus versus refinery runs — signaling opportunistic procurement and hedging against future volatility. That stockpiling strengthens Beijing’s energy security posture amid tight seasonal power markets.

Steel, industry—and policy cross-currents

Industrial curbs are real: coal and steel output dropped in August as Beijing enforced production controls to manage safety, prices, and emissions. But power demand records show the system still requires dispatchable capacity during climate-driven peaks, and policymakers are balancing those needs with selective supply restraint upstream.

What does China’s energy production means for industry?

- Coal: structurally constrained yet operationally indispensable during weather shocks; expect volatility around peaks, with policy steering annual totals.

- Hydro risk: multi-year hydrology remains the swing factor; poor inflows amplify thermal dispatch even as wind/solar expand.

- Renewables build-out: record power demand does not stall deployment; it raises the bar for storage, grid flexibility, and demand response to displace peak coal use over time. (Context: China’s rapid renewable scale-up alongside peak-season thermal reliance.)

- Commodities: peak-season coal burn supports seaborne prices; gas peaking demand adds optionality for LNG. Industrial caps temper raw-materials draw, but grid reliability imperatives keep thermal capacity investment live.

Bottom line

China’s record July load confirms an electrify-everything economy where dispatchable capacity still decides the last megawatt. Policy is cutting unsafe or excess coal mining even as the grid leans on thermal plants when hydro stumbles.